Understanding Credit Report. How to read it

Your credit report acts as a financial snapshot, detailing your credit history and influencing your

financial well-being. Knowing how to interpret this report empowers you to monitor your credit

health, identify potential issues, and take steps to improve your score.

Understanding the Sections:

Your credit report typically consists of the following sections:

- Personal Information: This section verifies your identity with details like your name, address, and Social Security number.

- Credit History: This is the most crucial section, listing all your credit accounts (credit cards, loans, etc.), their opening dates, credit limits, current balances, and payment history.

- Public Records: This section may include any bankruptcies, judgments, or tax liens filed against you.

- Credit Inquiries: This section lists inquiries made by lenders when you apply for credit, which can slightly impact your score.

Interpreting the Information:

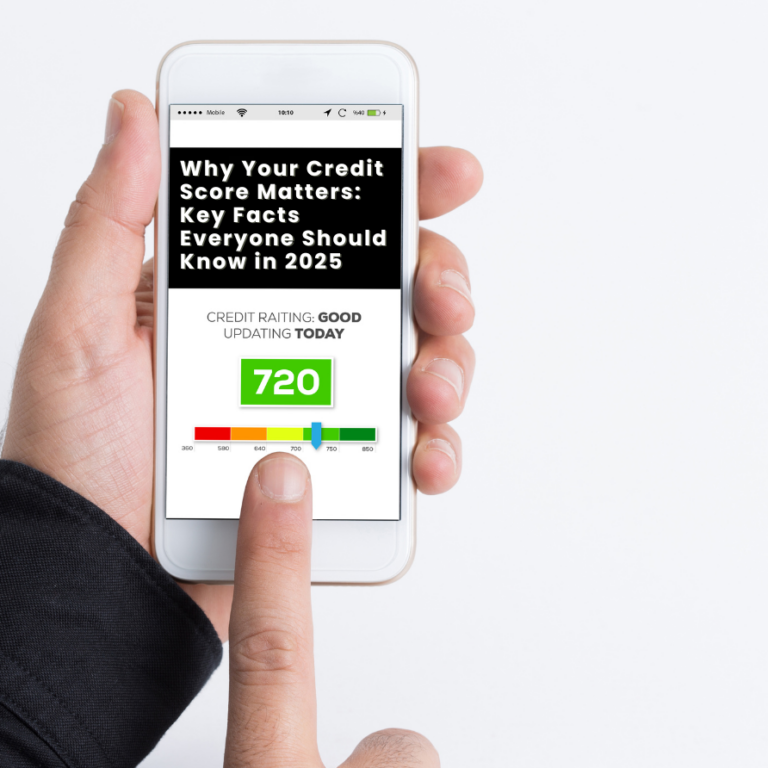

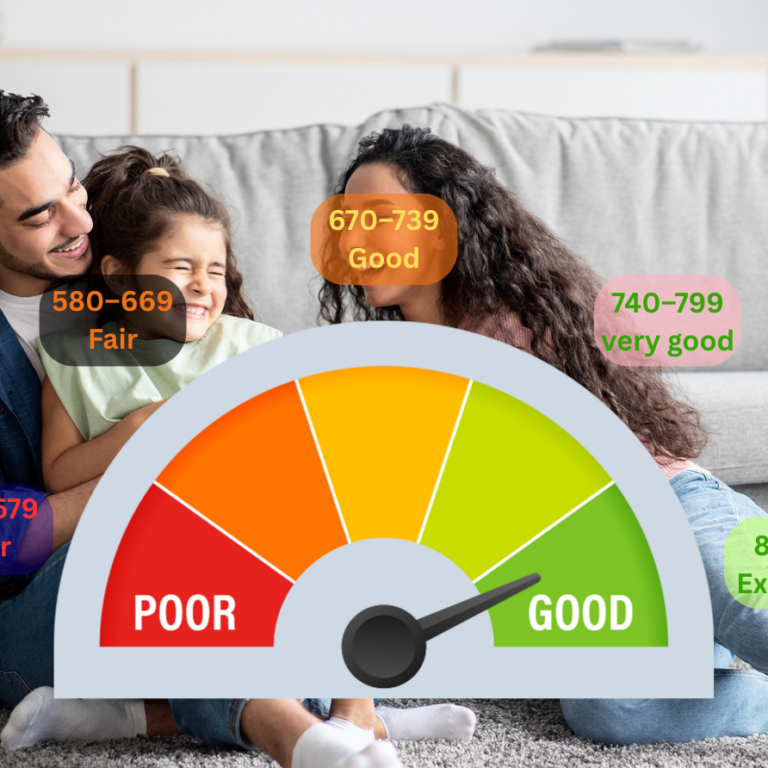

● Payment History: This is the single most important factor influencing your credit score.

Late payments or defaults significantly lower your score, while a consistent history of

on-time payments strengthens it.

● Credit Utilization: This refers to the amount of credit you’re using compared to your

available credit limit.Aiming for a utilization ratio below 30% shows responsible credit

management.

● Length of Credit History: A longer credit history generally indicates stability and

reliability, positively impacting your score.

● Credit Mix: Having a mix of credit types, such as credit cards and installment loans,

demonstrates responsible credit usage.

Identifying and Correcting Errors:

Review your credit report regularly for any inaccuracies or fraudulent activity. If you find errors,

dispute them directly with the credit bureau that reported them. You can access a free credit

report from each of the three major bureaus (Experian, Equifax, and TransUnion) annually

through AnnualCreditReport.com.

why is placing a fraud alert an effective way of dealing with inaccuracies in a credit report?

Placing a fraud alert is effective because it tells lenders to verify your identity before approving any new credit. So if there’s an inaccuracy—like an account you didn’t open—the alert helps stop more incorrect or fraudulent activity while you dispute the error. It adds a layer of protection and reduces the chance of further damage.

Resources:

● AnnualCreditReport.com: Provides free access to your credit reports from all three

major bureaus.

● Federal Trade Commission (FTC): Offers resources and guidance on disputing credit

report errors:https://consumer.ftc.gov/articles/disputing-errors-your-credit-reports

By understanding your credit report and taking proactive steps to maintain its accuracy, you can

build a strong credit foundation for a brighter financial future.