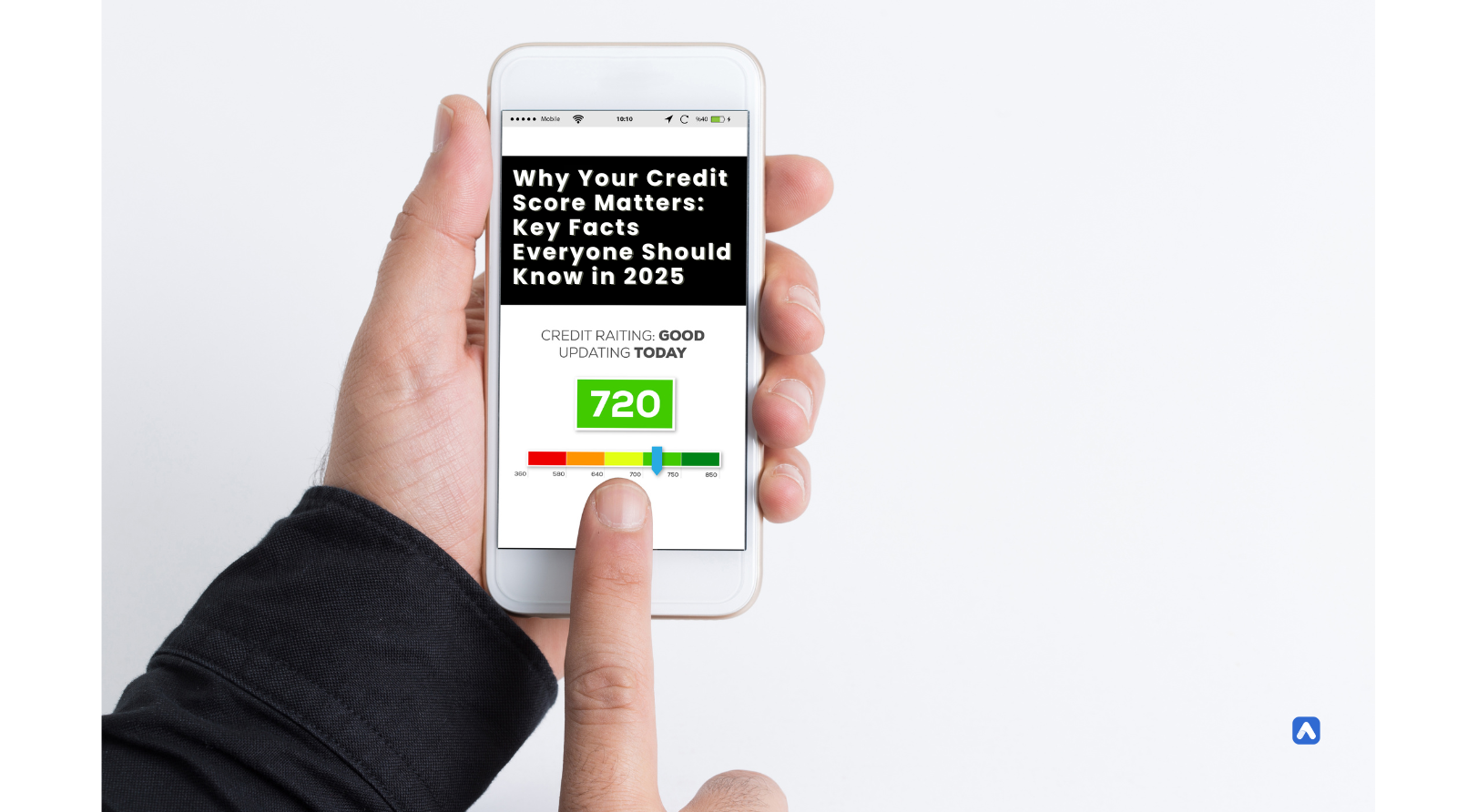

Why Your Credit Score Matters: Key Facts Everyone Should Know in 2025

Understanding Credit Scores: Definition and Importance

A credit score is a numerical representation of a person’s creditworthiness. It’s a three-digit number that lenders use to assess the likelihood of someone repaying a loan. This score is based on a variety of factors, including payment history, amounts owed, length of credit history, types of credit, and new credit.

The primary purpose of credit scores is to help lenders make informed decisions about whether or not to extend credit. A higher credit score generally indicates a lower risk of default, making it more likely that the lender will approve a loan request.

Credit Scores vs. Credit Reports: Key Differences Explained

While credit scores and credit reports are related, they are not the same thing.

In essence, a credit report provides the raw data, while a credit score is a calculated assessment of that data.

Why Credit Scores Matter: Their Significance for Consumers and Businesses

Credit scores have a significant impact on many aspects of a person’s financial life. A high credit score can lead to:

- Lower interest rates: When applying for loans, individuals with higher credit scores are often offered lower interest rates. This can result in significant savings over the life of a loan.

- Easier access to credit: Lenders are more likely to approve loan applications from individuals with good credit scores. This means that people with high scores have more options when it comes to borrowing money.

- Better terms on credit cards: Credit card companies often offer better terms, such as lower interest rates and higher credit limits, to customers with good credit.

- Lower insurance premiums: In some cases, individuals with good credit scores may qualify for lower insurance premiums.

For businesses, credit scores are equally important. They can help businesses assess the creditworthiness of potential customers and suppliers. This information can be used to make decisions about extending credit, setting credit limits, and managing risk.

History and Evolution of Credit Scores

The History of Credit Scoring: How Creditworthiness Was Assessed in the Past

The concept of assessing creditworthiness dates back centuries. In early civilizations, lenders relied on personal relationships and reputation to determine if borrowers were trustworthy. As societies grew more complex, more formal systems were developed to evaluate creditworthiness.

One notable early method was the use of character references. Potential borrowers would provide names of individuals who could vouch for their honesty and financial responsibility. Another method was to examine a person’s assets and liabilities. Those with significant assets and few debts were considered more likely to repay loans.

The FICO Score: How It Revolutionized Lending and Credit Decisions

The modern era of credit scoring began in the 1950s. In 1956, Fair Isaac and Company developed the Fair Isaac Score, which later became known as the FICO score. This scoring model used a mathematical algorithm to evaluate a person’s creditworthiness based on factors such as payment history, amounts owed, length of credit history, types of credit, and new credit.

The introduction of the FICO score revolutionized the lending industry. It provided lenders with a standardized and objective way to assess credit risk. As the FICO score became widely adopted, it became the de facto standard for credit scoring in the United States.

Evolution of Alternative Credit Scoring Models (e.g., VantageScore)

While the FICO score remains the most widely used credit scoring model, alternative models have also emerged. One notable example is the VantageScore, developed by a consortium of credit bureaus. VantageScore uses a different algorithm than FICO, but it assesses creditworthiness based on similar factors.

Alternative credit scoring models can be particularly useful for individuals who have limited or no credit history. These models may consider factors such as rent payments, utility bills, and cellphone bills to assess creditworthiness.

Key Legislation Shaping Credit Scoring: Impact of Acts Like the Equal Credit Opportunity Act

Several legislative acts have influenced the development and use of credit scoring. One of the most important is the Equal Credit Opportunity Act (ECOA). This law prohibits discrimination in credit transactions on the basis of race, color, religion, national origin, sex, marital status, age, or receipt of public assistance.

The ECOA has helped to ensure that credit scoring models are not biased against certain groups of people. It requires lenders to consider all relevant factors when evaluating creditworthiness, and it prohibits the use of discriminatory practices.

How Credit Scores Are Calculated

Understanding Credit Score Ranges: What Each Score Means

Credit scores typically range from 300 to 850, with higher scores indicating better creditworthiness. While the specific ranges may vary slightly between different scoring models, the general principle remains the same.

Key Factors Affecting Credit Scores

Credit scores are calculated based on five key factors:

- Payment History (35%): This is the most significant factor. On-time payments positively impact your credit score, while late or missed payments can negatively affect it.

- Credit Utilization (30%): This refers to the amount of credit you’re currently using compared to your total available credit. A high credit utilization ratio can negatively impact your score.

- Length of Credit History (15%): A longer credit history generally indicates a more established credit profile. Having older accounts can positively impact your score.

- Credit Mix (10%): Having a variety of credit accounts, such as credit cards, loans, and mortgages, can positively impact your score.

- New Credit (10%): Frequent applications for new credit can negatively impact your score, as it may signal increased risk.

How Credit Score Factors Are Weighted and How Models Differ

The weight of each factor in determining your credit score can vary across different scoring models. For example, some models may place a slightly higher emphasis on payment history, while others may give more weight to credit utilization.

Differences Between FICO and VantageScore Calculation Methods

While FICO and VantageScore both use similar factors to calculate credit scores, there are some key differences in their calculation methods:

It’s important to note that while the specific calculation methods may differ, the overall principles underlying credit scoring remain consistent across most models.

Types of Credit Scores

FICO Score

How FICO Scores Are Generated: FICO scores are calculated using a proprietary algorithm that takes into account five key factors: payment history, credit utilization, length of credit history, credit mix, and new credit. The specific weight given to each factor can vary depending on the specific FICO model being used.

Breakdown of FICO Score Ranges: FICO scores typically range from 300 to 850. While there’s no universally agreed-upon definition for each range, here’s a general breakdown:

VantageScore

Introduction and Differences from FICO: VantageScore is another widely used credit scoring model. It differs from FICO in several ways, including:

Common Use Cases for VantageScore: VantageScore is often used by lenders and credit bureaus. It can be particularly useful for individuals who have limited or no credit history, as it may consider factors such as rent payments and utility bills.

Specialty Credit Scores

Industry-Specific Scores (e.g., Auto, Mortgage): Some industries have developed specialized credit scores that are tailored to their specific needs. For example, auto lenders may use a credit score that places a greater emphasis on payment history for previous auto loans.

Use of Alternative Data for Scoring: In recent years, lenders have begun to experiment with alternative data sources to assess creditworthiness. This can include factors such as rent payments, utility bills, and even social media activity. These alternative data sources can be particularly useful for individuals who have limited or no credit history.

Custom Credit Scores

Proprietary Scores Used by Banks and Lenders: Many banks and lenders develop their own proprietary credit scoring models. These models may incorporate factors that are specific to the lender’s business or target market.

Differences Between Publicly Available and Private Scores: Publicly available credit scores, such as FICO and VantageScore, are generally available to consumers. Private scores, on the other hand, are only available to lenders or other authorized parties. These scores may be more detailed or may incorporate factors that are not included in publicly available scores

The Impact of Credit Scores on Consumers: How Your Score Affects Your Financial Life

Impact on Loan and Credit Card Approvals

A high credit score is generally a prerequisite for obtaining loans and credit cards. Lenders view individuals with good credit scores as less risky borrowers, making them more likely to approve loan applications and offer favorable terms.

Influence on Interest Rates, Insurance Premiums, and Rental Agreements

Individuals with high credit scores often qualify for lower interest rates on loans and credit cards. Additionally, insurance companies may offer lower premiums to policyholders with good credit scores. In some cases, landlords may consider credit scores when evaluating rental applications.

Employment Screening and Credit Score Usage

While the practice of using credit scores for employment screening has been controversial, it’s still used by some employers. Proponents argue that credit scores can provide insights into a person’s financial responsibility and work ethic.However, critics contend that credit scores can be biased against certain groups of people and may not be a reliable indicator of job performance.

Interpreting Your Credit Score: What It Means for Your Financial Health

Understanding your credit score is essential for managing your financial health. Here are some key points to remember:

- Know your score: Regularly check your credit report and score to stay informed.

- Understand the factors: Be aware of the five key factors that influence your credit score.

- Monitor your credit activity: Keep track of your credit card balances, payments, and new credit inquiries.

- Dispute errors: If you find any errors on your credit report, dispute them promptly.

- Improve your score: If your credit score is low, take steps to improve it, such as paying bills on time, reducing debt, and avoiding unnecessary credit inquiries.

By understanding how credit scores work and taking steps to improve yours, you can enhance your financial well-being and access more opportunities.

How Credit Scores Impact Businesses

Assessing Borrower Risk Using Credit Scores

Businesses rely heavily on credit scores to assess the risk associated with lending money to customers. A high credit score indicates a lower likelihood of default, making the borrower more attractive to lenders.

The Role of Credit Scores in B2B Lending: Driving Business Financing Decisions

In business-to-business (B2B) lending, credit scores are used to evaluate the financial health and creditworthiness of businesses. This information helps lenders determine the risk associated with extending credit to a company.

The Role of Credit Scores in Customer Segmentation and Pricing Models

Businesses can use credit scores to segment customers into different risk categories. This information can be used to tailor pricing models and credit terms to specific customer segments. For example, customers with high credit scores may be offered lower interest rates and more favorable terms.

Regulatory Requirements for Businesses Using Credit Scores (e.g., Fair Credit Reporting Act)

Businesses that use credit scores must comply with various regulatory requirements, such as the Fair Credit Reporting Act (FCRA). The FCRA protects consumers’ rights and ensures that credit information is handled responsibly.

Credit Score Ranges Explained: Understanding Their Significance

Excellent Credit (750–850): Benefits and Opportunities

Individuals with excellent credit scores have access to a wide range of credit products, including loans, credit cards, and mortgages. They typically qualify for lower interest rates and more favorable terms.

Good Credit (700–749): Access to Most Credit Products

Individuals with good credit scores can usually obtain most credit products, but they may face higher interest rates and less favorable terms compared to those with excellent credit.

Fair Credit (650–699): Higher Interest Rates and Limited Credit Access

Individuals with fair credit may have limited access to credit or may be offered higher interest rates. They may also face restrictions on the types of credit products available to them.

Poor Credit (600–649): Limited Access to Credit and Higher Fees

Individuals with poor credit may have difficulty obtaining credit or may be offered limited options. They may also face higher interest rates and fees.

Very Poor Credit (300–599): Significant Financial Barriers

Individuals with very poor credit may have significant financial barriers. They may find it difficult to obtain credit or may be required to pay exorbitant interest rates and fees.

Improving and Maintaining Your Credit Score

Effective Strategies to Boost Your Credit Score

- Paying Bills on Time: This is the most crucial step. Consistent on-time payments demonstrate financial responsibility and positively impact your credit score.

- Reducing Credit Utilization: Keep your credit card balances low compared to your credit limits. A high credit utilization ratio can negatively affect your score.

- Avoiding New Credit Applications: Frequent applications for new credit can lower your score. Only apply for credit when necessary.

- The Importance of Regular Credit Monitoring: Regularly check your credit report to ensure accuracy and identify any errors. This can help protect your credit score.

- Disputing Errors on Your Credit Report: If you find errors on your credit report, dispute them promptly. Incorrect information can negatively impact your score.

Tips for Sustaining Strong Credit Health Long-Term

- Continue making on-time payments: Consistent on-time payments are essential for maintaining a good credit score.

- Manage your credit utilization: Keep your credit card balances low to avoid high credit utilization ratios.

- Limit new credit: Only apply for new credit when necessary to avoid unnecessary inquiries.

- Monitor your credit report regularly: Check your credit report at least once a year to identify any errors or fraudulent activity.

- Dispute errors promptly: If you find errors on your credit report, take immediate action to dispute them.

- Consider a credit counseling service: If you’re struggling with debt or have questions about credit management, consider consulting with a credit counseling service.

The Role of Alternative Data in Credit Scoring

What Is Alternative Data?

Alternative data refers to information that is not typically included in traditional credit reports, such as rent payments, utility bills, and cellphone bills. This type of data can provide a more comprehensive picture of a person’s financial behavior.

How Alternative Data Benefits Consumers with Limited Credit Histories

For individuals with limited or no credit history, alternative data can be particularly beneficial. By considering factors such as rent payments and utility bills, lenders can gain a better understanding of a person’s financial responsibility and make more informed credit decisions.

Risks and Challenges of Alternative Data Usage

While alternative data can be valuable, it also poses some risks and challenges. One concern is the potential for bias in the data. If alternative data is not collected and analyzed in a fair and equitable manner, it could perpetuate existing inequalities. Additionally, there may be privacy concerns associated with the use of alternative data.

Case Studies of Successful Alternative Credit Models

1. Rent Reporting Companies

2. Utility Payment Reporting Companies

3. Fintech Startups

4. Mobile Payment Apps

These case studies demonstrate the potential of alternative credit models to provide access to credit for individuals who may have difficulty obtaining traditional financing. By incorporating alternative data, these companies have been able to make more informed credit decisions and help people build their credit histories

Modern Credit Scoring Trends and Innovations

The Rise of Real-Time Credit Scoring Models

Real-time credit scoring models allow lenders to assess creditworthiness instantly, enabling faster and more efficient decision-making. This is particularly beneficial for industries like retail and e-commerce, where quick approvals are essential.

Use of Artificial Intelligence and Machine Learning in Credit Scoring

Artificial intelligence (AI) and machine learning (ML) are being used to develop more sophisticated credit scoring models. These technologies can analyze vast amounts of data to identify patterns and trends that may not be apparent to human analysts.

Blockchain and Decentralized Credit Scores

Blockchain technology has the potential to revolutionize credit scoring by creating decentralized and transparent systems. Decentralized credit scores could provide individuals with greater control over their credit data and reduce the risk of data breaches.

Predictive Credit Models and Their Impact on Risk Management

Predictive credit models use advanced analytics to forecast future credit behavior. This can help lenders identify potential risks early on and take proactive measures to mitigate them.

The Push for Financial Inclusion Through Alternative Credit Models

Alternative credit models are playing a crucial role in promoting financial inclusion. By considering factors beyond traditional credit history, these models can help individuals with limited or no credit history access credit.

Global Credit Scoring Practices

Credit Scoring Systems Around the World

Credit scoring systems vary significantly across different countries. For example, the United States primarily uses FICO scores, while the United Kingdom uses a variety of scoring models. In China, a different credit scoring system is used, often based on social behavior and payment history. Emerging markets may have less developed credit scoring systems or may rely heavily on personal relationships and collateral.

Differences in Credit Scoring Criteria Across Regions

The criteria used to calculate credit scores can vary across regions. In some countries, payment history may be the most important factor, while in others, credit utilization or length of credit history may be given more weight. Cultural differences and economic conditions can also influence credit scoring practices.

The Challenges of Cross-Border Credit Scoring

Cross-border credit scoring can be challenging due to differences in data availability, regulations, and cultural norms. Lenders may need to adapt their credit scoring models to account for these variations.

Efforts to Standardize Global Credit Reporting and Scoring Practices

There have been efforts to standardize global credit reporting and scoring practices. Organizations like the Credit Bureau International (CBI) and the International Organization for Standardization (ISO) have developed guidelines and standards to promote consistency and interoperability. However, significant challenges remain, as countries have different legal and regulatory frameworks

Controversies and Challenges in Credit Scoring

Bias and Discrimination

Racial and Socioeconomic Bias in Credit Scoring Models: One of the most significant controversies surrounding credit scoring is the potential for bias. Studies have shown that credit scoring models can disproportionately affect certain groups, such as racial minorities and low-income individuals. This can lead to systemic discrimination and limit access to credit.

Efforts to Mitigate Discriminatory Practices: To address these concerns, regulators and industry leaders have implemented measures to mitigate discriminatory practices in credit scoring. These efforts include:

Data Privacy Concerns

Security of Consumer Credit Data: Credit data is highly sensitive and valuable. The security of this data is a major concern. Data breaches and identity theft can have severe financial consequences for consumers.

Regulatory Efforts to Protect Personal Information: To protect consumer privacy, governments have enacted regulations such as the Fair Credit Reporting Act (FCRA) and the General Data Protection Regulation (GDPR). These laws require businesses to implement measures to safeguard consumer data and provide individuals with greater control over their personal information.

Over-Reliance on Traditional Credit Scores

Financial Exclusion of Underserved Populations: The over-reliance on traditional credit scores can lead to financial exclusion for underserved populations, such as individuals with limited or no credit history. These individuals may be unable to obtain credit, even if they are financially responsible.

The Debate Over Alternative Data and Scoring Models: Alternative credit models that incorporate factors beyond traditional credit history can help address the issue of financial exclusion. However, there is ongoing debate about the effectiveness and fairness of these models. Some critics argue that alternative data can also be biased, while others believe that it can provide a more accurate assessment of creditworthiness.

The Future of Credit Scores

Trends Shaping the Future of Credit Scoring

- AI, Big Data, and Predictive Analytics: The increasing availability of data and advancements in AI and machine learning are driving the development of more sophisticated credit scoring models. These models can analyze vast amounts of data to identify patterns and trends that may not be apparent to human analysts.

- Decentralization and Consumer-Controlled Credit Data: Blockchain technology has the potential to revolutionize credit scoring by creating decentralized and transparent systems. This could give consumers greater control over their credit data and reduce the risk of data breaches.

- Global Adoption of Alternative Credit Models: Alternative credit models are gaining traction in many countries, particularly in emerging markets. As these models become more widely adopted, they could help to improve financial inclusion and reduce the reliance on traditional credit scores.

Anticipated Legislative and Regulatory Changes

- Data Privacy: As concerns about data privacy continue to grow, we can expect stricter regulations governing the collection and use of credit data.

- Financial Inclusion: Governments may implement policies to promote financial inclusion, which could include initiatives to expand access to credit for underserved populations.

- Bias and Discrimination: Efforts to address bias in credit scoring models are likely to continue. Regulators and industry leaders may implement new measures to ensure fairness and transparency.

The Evolution of Credit Scoring Through Financial Inclusion Initiatives

Financial inclusion initiatives, such as the expansion of access to credit for underserved populations, will likely have a significant impact on credit scoring. As more individuals build credit histories, the credit scoring landscape will evolve.

Practical Tips for Consumers

Decoding Your Credit Score: What You Need to Know

Starting Fresh: Strategies for Building and Rebuilding Your Credit

Avoiding Common Pitfalls that Harm Credit Scores

Practical Tips for Businesses

Conclusion

Essential Insights: Key Takeaways on Credit Scores

- Importance of Credit Scores in Financial Decision-Making: Credit scores play a crucial role in various financial decisions, including loan approvals, interest rates, insurance premiums, and rental agreements. A good credit score can open up many opportunities, while a poor credit score can limit financial options.

- Proactive Credit Score Management for Consumers and Businesses: Individuals and businesses should take a proactive approach to managing their credit scores. This involves understanding the factors that influence credit scores, monitoring credit reports regularly, and taking steps to improve creditworthiness.

- Future Outlook: Evolution of Credit Scoring Systems and Financial Inclusion: The future of credit scoring is likely to be shaped by technological advancements, regulatory changes, and the growing emphasis on financial inclusion. Alternative credit models, AI, and blockchain technology are expected to play a significant role in reshaping the credit scoring landscape.

Final Thoughts: How Credit Awareness Fuels Financial Empowerment and Stability

Credit awareness is essential for financial empowerment. By understanding how credit scores work and taking steps to improve them, individuals and businesses can make more informed financial decisions and achieve their goals. A strong credit score can provide a solid foundation for financial stability and can open up a wide range of opportunities.