Stop Credit Damage: How to Contact the Company That Made a Hard Inquiry

Spotting a suspicious hard inquiry on your credit report can feel like a red flag — and for good reason. Hard inquiries, especially those you didn’t authorize, can affect your credit score and hint at potential fraud. While filing a dispute with the credit bureaus is one route, contacting the company that made a hard inquiry directly can often fast-track the removal process.

In this guide, we’ll walk you through why reaching out to the creditor matters, how to contact them, what to ask for, and how this fits into your overall dispute strategy.

Why Contacting the Creditor Matters ?

It might seem easier to go straight to the credit bureau — and that’s a valid step — but contacting the company that made the inquiry can often be faster and more effective. Here’s why:

- The credit bureaus rely on the furnisher of the information (in this case, the company) to verify whether a hard inquiry is valid.

- If the company confirms the inquiry was a mistake, they can directly request the bureau to remove it.

- Getting a written acknowledgment or correction from the creditor can strengthen your case if you choose to dispute the inquiry through a bureau.

Think of this as getting the source to confirm the error — it speeds things up and makes your argument bulletproof.

How to Reach Out to the Creditor

Once you’ve identified the company that placed the hard inquiry, the next step is to contact them. This can be done in a few different ways depending on your preference and urgency.

1. Phone Call (Good for Immediate Clarification)

- Call the company’s customer service or credit department.

- Ask to speak with someone regarding a hard inquiry on your credit report.

- Have your credit report in front of you so you can reference the date and name of the inquiry.

Tip: Always write down the date, time, and name of the representative you spoke with for your records.

2. Email (Good for Written Responses)

- Check the company’s website for a contact email related to credit, billing, or support.

- Send a polite but clear message outlining the situation and requesting clarification or removal.

3. Certified Mail (Best for Formal Disputes)

- For serious matters or if you’re not getting a response via phone/email, send a certified letter with a return receipt.

- This ensures there’s a paper trail showing that the company received your request.

Finding the Right Contact Information

Sometimes, the name of the company listed in the inquiry isn’t immediately familiar. Here’s how to find the right contact:

- Google the name exactly as it appears on your credit report. Many creditors use formal or abbreviated business names.

- Check your credit card or loan statements if you suspect it’s a company you’ve worked with.

- Use directories like Better Business Bureau (BBB) or LinkedIn to find company contacts.

- Call the credit bureau and ask for the contact information of the creditor that reported the inquiry.

What to Request from the Creditor

Once you’re in touch with the company, here’s what you should ask for:

1. A Copy of the Credit Application

Ask if they have a signed application or digital record showing that you authorized the inquiry. If they can’t provide it, the inquiry may be invalid.

2. Written Acknowledgment of the Error

If they agree that the inquiry was placed in error or due to identity theft, request that they send you written confirmation.

3. Formal Request for Removal

Ask them to contact the credit bureaus directly to request removal of the inquiry.

Sample Letter You Can Use:

Subject: Request to Remove Unauthorized Hard Inquiry

Dear [Company Name],

I recently reviewed my credit report and noticed a hard inquiry made by your organization on [Date]. I do not recall applying for credit with your company and did not authorize this inquiry.

I am requesting the following:

- A copy of the credit application or authorization form

- A written acknowledgment if this inquiry was made in error

- That you notify the credit bureaus to have this inquiry removed immediately

Please consider this a formal request under the Fair Credit Reporting Act (FCRA). I’ve included a copy of my credit report highlighting the inquiry, as well as proof of my identity.

Thank you for your prompt attention to this matter.

Sincerely,

[Your Name]

[Your Address]

[Your Contact Info]

What If the Creditor Refuses to Remove the Inquiry?

Sometimes, the company may insist the inquiry was authorized — even if you disagree. If that happens, you still have options.

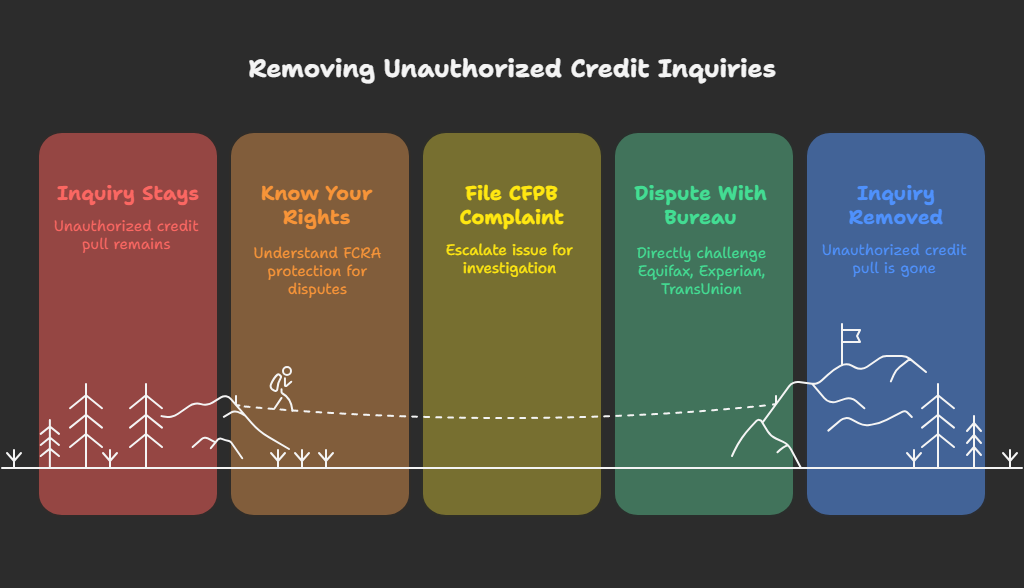

Know Your Rights Under the FCRA

The Fair Credit Reporting Act protects your right to dispute inaccurate or unauthorized credit report entries. If a creditor can’t prove you authorized a hard inquiry, they are legally obligated to remove it.

File a Complaint with the CFPB

If the company is unresponsive or refuses to cooperate, you can file a formal complaint with the Consumer Financial Protection Bureau (CFPB) at:

They will reach out to the company and help investigate your case.

Dispute Directly With the Credit Bureau

If the company won’t help, you can still submit your own dispute to Equifax, Experian, or TransUnion. Be sure to include any correspondence you had with the creditor — it will strengthen your case.

How This Impacts the Dispute Process

Contacting the company directly can make a huge difference in the outcome of your credit dispute.

- If the creditor confirms the inquiry was an error and contacts the bureau, the entry may be removed within days.

- If you’re filing a dispute with a bureau and you already have written proof from the company, you’re much more likely to succeed.

- This approach can also protect you from future unauthorized inquiries if the issue was part of a larger fraud pattern.

Final Thoughts: Don’t Ignore a Bad Inquiry — Take Action

Hard inquiries aren’t just small blemishes on your credit — they can impact your score and even signal bigger problems like identity theft. By taking the time to contact the company that placed the inquiry, you can potentially get it removed faster and more efficiently than waiting on a credit bureau.

Be polite, be persistent, and always keep documentation of every interaction. In many cases, a simple conversation can lead to a clean credit report — and peace of mind.