Does a mortgage inquiry affect credit score ?

You know you need to shop around for the best mortgage rate, but every time a lender pulls your credit, you fear your FICO score will plummet. This fear is rooted in a fundamental misunderstanding of how the credit scoring system handles rate shopping for major loans.

The short answer is: Yes, a mortgage inquiry is a Hard Inquiry, but the impact on your score is minimal and temporary, provided you follow the rules.

This article will break down what a mortgage inquiry is, how it appears on your credit report, and the essential “shopping window” FICO gives you to secure the best loan without penalty.

What is a Mortgage Inquiry?

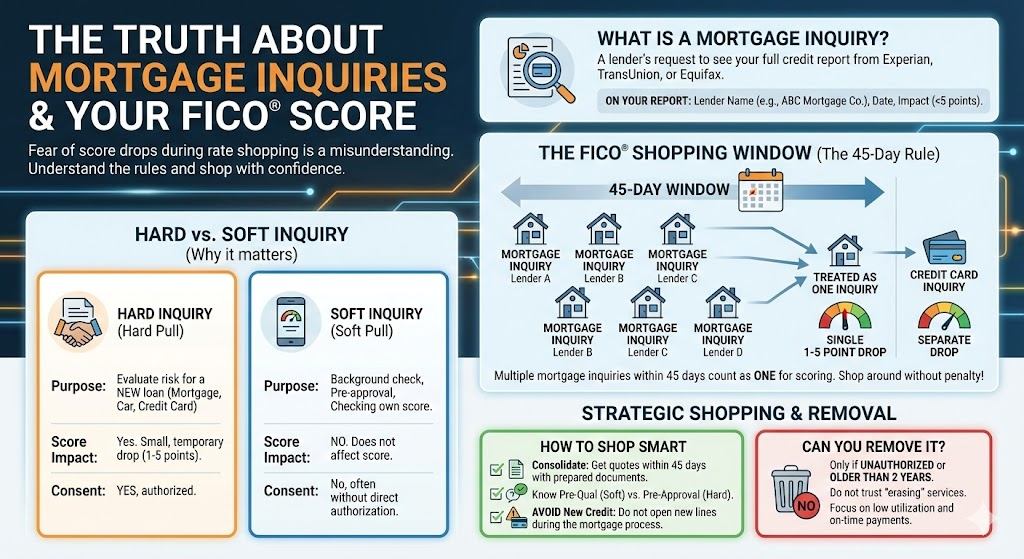

A mortgage inquiry is simply a request made by a potential lender to one or more of the three major credit bureaus (Experian, TransUnion, Equifax) to view your full credit report and credit score.

Mortgage Inquiry on Credit Report

Every mortgage inquiry will appear on your credit report, listed under the “Inquiries” section.

- Lender Name: It will list the name of the lender or broker who initiated the request (e.g., “ABC Mortgage Company”).

- Date: It will show the exact date the request was made.

- Impact: A single inquiry typically causes a drop of less than 5 points on your FICO Score.

Is a Mortgage Inquiry a Hard Inquiry? (And Why it Matters)

Yes, a mortgage inquiry is a Hard Inquiry, also known as a hard pull.

When you apply for credit—any type of credit, including a mortgage, car loan, or credit card—the lender is assessing the risk of extending you money. This process requires a Hard Inquiry.

Hard Inquiry vs. Soft Inquiry

| Feature | Hard Inquiry (Hard Pull) | Soft Inquiry (Soft Pull) |

|---|---|---|

| Purpose | To evaluate risk for a new loan or credit account. | Background check, pre-approved offers, or checking your own score. |

| Credit Score Impact | Yes. Causes a small, temporary dip (typically 1–5 points). | No. Does not affect your credit score. |

| Consent Required | Yes, you must authorize it. | No, often done without direct authorization. |

| Example | Applying for a mortgage, car loan, or credit card. | Checking your score on a banking app or getting an insurance quote. |

The FICO Rule: The Mortgage Rate Shopping Window

If every hard inquiry caused a 5-point drop, shopping around for the best mortgage rate (which requires checking with 3-5 lenders) would severely damage your score. FICO is designed to prevent this penalty, recognizing that comparison shopping is necessary and responsible behavior.

The FICO De-Duplication Rule

FICO models (including the current FICO 8 and the forthcoming FICO 10 G) have a special mechanism to handle multiple inquiries for the same loan purpose within a specific time frame.

The Shopping Window:

- What Counts: All mortgage inquiries that occur within a 45-day window are treated as a single inquiry for scoring purposes.

- The Benefit: You can shop with four or five different lenders over a month, and your credit score will only be affected once, by that initial 1–5 point drop.

- What Does Not Count: If you apply for a credit card and a mortgage in the same window, the credit card inquiry will be treated separately because it is a different loan type.

This rule is designed to encourage consumers to find the lowest interest rate and prevent a predatory market where shoppers are afraid to look beyond the first quote.

How to Strategically Shop for a Mortgage

To maximize the benefit of the FICO shopping window and minimize impact:

1. Consolidate Your Shopping

Before you begin shopping, make sure you have all your necessary financial documents ready (W-2s, pay stubs, bank statements). Once you start, aim to get rate quotes and pre-approvals from all your desired lenders within the 45-day window.

2. Know the Difference Between Pre-Qualification and Pre-Approval

- Pre-Qualification: This is often a soft inquiry (or no inquiry at all). You provide basic financial information, and the lender gives you an estimate of what you can afford. This does not lock in a rate.

- Pre-Approval: This requires a Hard Inquiry. The lender pulls your full report to verify your debt and score, and they issue you a commitment letter with a specific loan amount and a rate based on that date. This is the stage that matters most for your credit.

3. Avoid New Credit During the Process

Do not open a new credit card, take out a car loan, or finance furniture during the 60–90 days leading up to, and during, your mortgage application process. Any new credit line will reset your inquiry count and alter your Debt-to-Income (DTI) ratio, potentially jeopardizing your final loan approval.

How to Remove Mortgage Inquiry from Credit Report

A hard inquiry cannot be “removed” from your credit report unless it meets one of two criteria:

- It is over two years old: Hard inquiries automatically drop off your credit report after 24 months. By this point, they no longer affect your FICO score.

- It was unauthorized: If a lender pulled your credit report without your explicit written permission (which is rare in the mortgage industry), you can file a dispute with the credit bureau to have it removed.

Important: Do not trust third-party services that promise to “erase” hard inquiries immediately. Unless the inquiry was fraudulent, you must wait for the two-year period to pass. Since mortgage inquiries within the 45-day window have a minimal impact anyway, attempting to remove them is often not worth the effort.

By understanding the FICO shopping window, you can confidently shop for the best mortgage rate without the fear of damaging your credit score. Focus on what truly matters: keeping your utilization low and paying every bill on time.

FAQs

1. Do mortgage inquiries hurt my credit score?

Only slightly—usually 1–5 points—and the effect is temporary.

2. Are mortgage inquiries hard pulls?

Yes, mortgage checks are hard inquiries.

3. Will multiple lenders checking my credit lower my score?

No—FICO counts all mortgage inquiries within 45 days as one.

4. How long do mortgage inquiries stay on my report?

They remain for 2 years but stop affecting your score after about 12 months.

5. Can I remove a mortgage inquiry?

Only if it’s unauthorized; otherwise, it naturally drops off after two years.