FICO Score Versions: which is used for mortgage ?

You check your credit score on your banking app, and it says 720. You go to buy a car, and the dealer tells you your score is 705. You apply for a mortgage, and the lender says your middle score is 680.

You are not crazy, and the system isn’t broken. You just have different versions of your FICO® Score.

Think of FICO scores like iPhones or Windows operating systems. Just as you might be using an iPhone 15 while your friend is still on an iPhone 12, lenders use different “versions” of the FICO scoring model depending on their industry and their technology.

Currently, there are over 28 different FICO scores attached to your name. Understanding which one matters is the key to mastering your financial life.

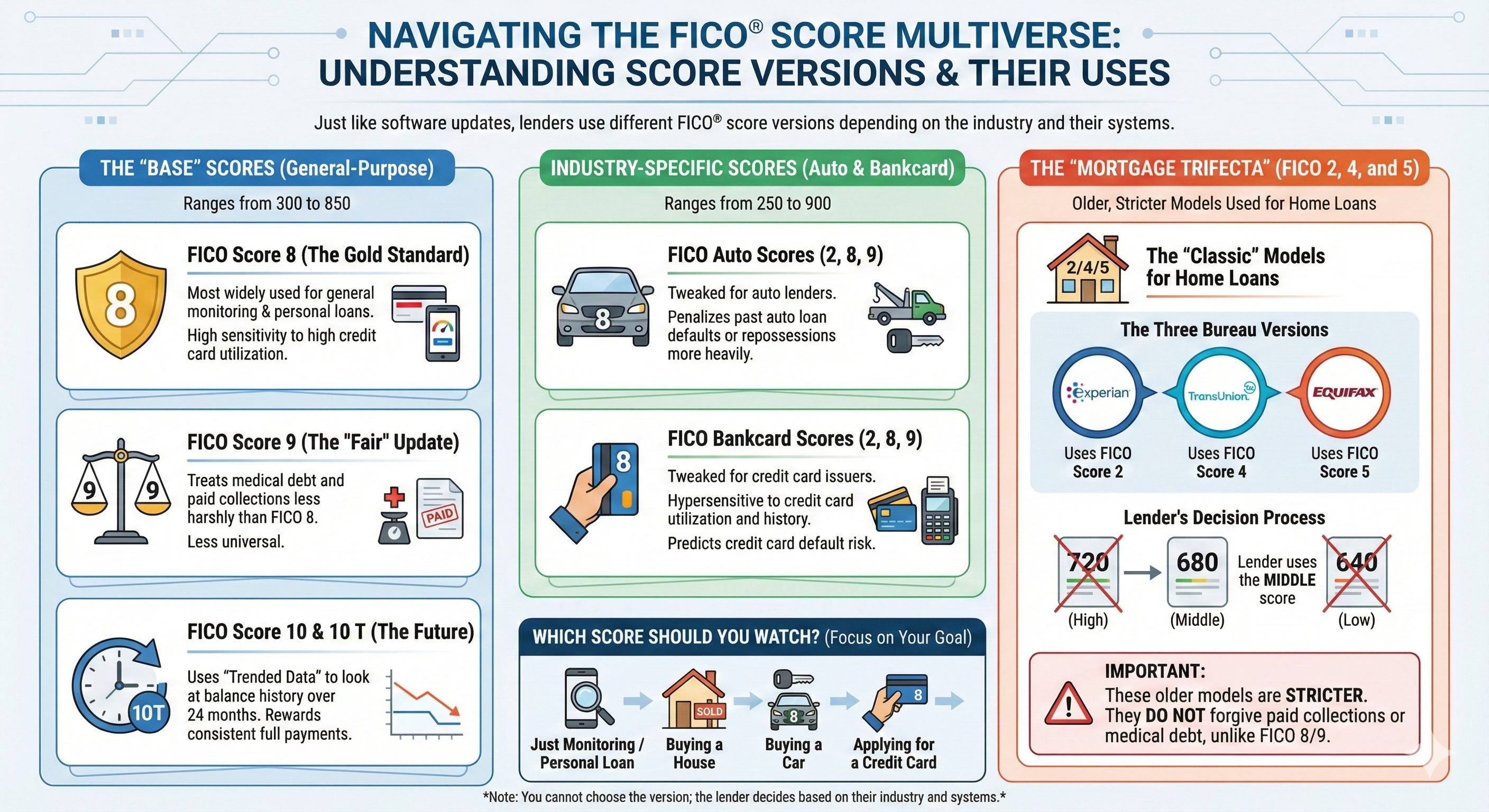

The “Base” Scores: FICO 8, 9, and 10

These are the general-purpose scores used for basic lending decisions. They range from 300 to 850.

1. FICO Score 8 (The Gold Standard)

This is the most widely used score in the world. If you check your credit on a free app or apply for a personal loan, this is likely the number being used.

- Key Feature: High sensitivity to high credit card utilization.

2. FICO Score 9 (The “Fair” Update)

Released to help consumers, this version treats debt differently.

- Medical Debt: Unpaid medical bills have less impact than other debts.

- Paid Collections: If you pay off a collections account in full, FICO 9 ignores it (unlike FICO 8, which still counts it against you).

- Adoption: Used by some lenders, but not as universal as FICO 8 yet.

3. FICO Score 10 & 10 T (The Future)

The “T” stands for Trended Data.

- Trended Data: Previous models only looked at your balance today. FICO 10 T looks at your balance history over the last 24 months.

- Why it matters: If you pay off your credit card in full every month, FICO 10 T rewards you more than someone who carries a balance, even if your utilization is the same on the day the snapshot is taken.

The Industry-Specific Scores (Auto & Bankcard)

When you apply for a car loan or a credit card, lenders don’t always use the “Base” score. They use a version tweaked to predict specific risks. These scores have a different range: 250 to 900.

FICO Auto Scores (2, 8, 9)

Designed for auto lenders.

- The Logic: This algorithm penalizes you more heavily for past auto loan defaults or repossession. It is specifically looking for the risk that you won’t pay for your car.

FICO Bankcard Scores (2, 8, 9)

Designed for credit card issuers (Chase, Amex, Citi).

- The Logic: This version is hypersensitive to credit card utilization and history. It predicts the likelihood that you will default on a credit card specifically.

The “Mortgage Trifecta”: FICO 2, 4, and 5

This is the most critical category. While the rest of the world has moved on to FICO 8 or 9, the mortgage industry is stuck in the past.

Because most mortgages are sold to government-backed entities (Fannie Mae and Freddie Mac), lenders are required to use older, stricter versions of FICO.

The “Classic” Models:

- Experian: Uses FICO Score 2.

- TransUnion: Uses FICO Score 4.

- Equifax: Uses FICO Score 5.

When you apply for a home loan, the lender pulls all three of these old scores. They ignore the highest, ignore the lowest, and use the middle number to determine your interest rate.

Important: These older models do not forgive paid collections or medical debt. They are much stricter than the FICO 8 score you see on your phone.

Which Score Should You Watch?

You cannot possibly monitor all 28 scores at once. Focus on the one relevant to your next big goal.

| Your Goal | The Score That Matters |

|---|---|

| Just Monitoring / Personal Loan | FICO Score 8 (General) |

| Buying a House | FICO 2, 4, 5 (Mortgage) |

| Buying a Car | FICO Auto Score 8 |

| Applying for a Credit Card | FICO Bankcard Score 8 |

Frequently Asked Questions (FAQ)

Which FICO score is used for mortgages?

Mortgage lenders typically use older FICO versions known as the ‘Classic’ models: FICO Score 2 (Experian), FICO Score 5 (Equifax), and FICO Score 4 (TransUnion).

Why is my FICO 8 higher than my Mortgage Score?

FICO 8 is more forgiving. It treats isolated mistakes (like small collections) less harshly than the older FICO 2/4/5 mortgage models. It is common for your “Mortgage Score” to be 20–40 points lower than your “App Score.”

Can I upgrade my score to FICO 10?

No. You cannot choose which version is used. The lender decides which software version they want to pay for. Most lenders are slow to upgrade because their entire risk system is built around the older models.

Does paying off collections help my Mortgage FICO score?

Usually, no. The older FICO 2, 4, and 5 models see a “paid collection” the same as an “unpaid collection”—it is still a major negative mark. However, paying it off does look better to the human underwriter reviewing your file, even if the score number doesn’t change.

How do I see my Mortgage Scores?

Most free credit apps (like Credit Karma) show VantageScore, not FICO. To see your specific FICO 2, 4, and 5 scores, you usually have to pay for a subscription directly from myFICO.com or Experian.com, as these are premium data points.