Found an Error on Your Credit Report? Here’s What to Do

Discovering a mistake on your credit report is terrifying. Whether it is a stranger’s credit card listed under your name or a bill you paid three years ago showing up as “unpaid,” these errors can unfairly tank your credit score by 50 to 100 points.

You are not alone. A study by the Federal Trade Commission (FTC) found that one in five Americans has a material error on their credit report.

The good news is that the law is on your side. Under the Fair Credit Reporting Act (FCRA), credit bureaus must prove that the data they report is accurate. If they can’t prove it, they must delete it.

Here is the step-by-step guide on what to do if you find an error on your credit report.

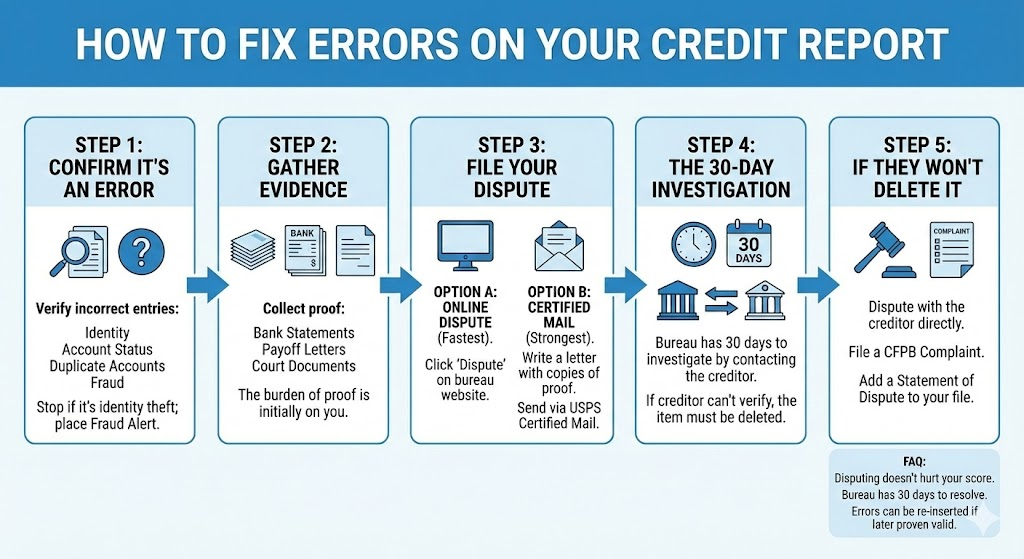

Step 1: Confirm It Is Actually an Error

Before you panic, verify that the entry is truly incorrect.

- Identity Errors: Is your name misspelled? Is there an address listed where you never lived? (Common if you have a common name like “John Smith”).

- Account Status Errors: Is a closed account listed as open? Is a paid-off loan listed as unpaid?

- Duplicate Accounts: Is the same debt listed twice? (e.g., once by the original bank and once by a collection agency).

- Fraud: Is there an account you never opened? Stop here. This is identity theft. You need to place a Fraud Alert immediately at IdentityTheft.gov.

Step 2: Gather Your Evidence

You cannot just say, “This is wrong.” You need receipts. The burden of proof is initially on you to show why the report is inaccurate.

- Bank Statements: Showing the payment clearing your account.

- Payoff Letters: A letter from the lender stating the account was paid in full.

- Court Documents: If a judgment or bankruptcy was dismissed.

Step 3: File Your Dispute (The Right Way)

You have two options for filing a dispute. While the “Online” button is easier, the “Certified Mail” method is legally safer.

Option A: The Online Dispute (Fastest)

Every bureau allows you to click “Dispute” next to an item on their website.

- Pros: Fast, free, and easy.

- Cons: You often waive the right to sue by accepting their online Terms of Service. It can also be harder to upload complex evidence.

Option B: Certified Mail (Strongest)

This creates a paper trail that holds up in court. You write a letter clearly stating the error and attach copies (never originals) of your proof.

- Send to: Equifax, Experian, and TransUnion (whoever is reporting the error).

- The “Certified” Part: Send it via USPS Certified Mail with Return Receipt Requested. This gives you legal proof of the exact date they received it.

Step 4: The 30-Day Investigation Window

Once the bureau receives your dispute, the clock starts. By federal law (FCRA), they have 30 days to investigate.

- They contact the creditor: They ask the bank, “Hey, this person says they paid this bill. Do you have proof they didn’t?”

- The creditor checks records: If the creditor cannot verify the debt or fails to respond within the window, the bureau must delete the item.

- The Result: You will receive a notification stating the item was either “Deleted,” “Updated,” or “Verified” (meaning they believe it is accurate).

Step 5: What If They Won’t Delete It?

If the bureau responds with “Verified” but you know you are right, do not give up.

- Dispute with the Creditor: Contact the bank or collection agency directly. Send them the same proof you sent the bureau.

- File a CFPB Complaint: The Consumer Financial Protection Bureau (CFPB) oversees credit reporting. Filing a complaint on consumerfinance.gov usually gets a response from the bureau’s high-level escalation team within 15 days.

- Add a Statement of Dispute: You can ask the bureau to add a 100-word note to your file explaining your side of the story (e.g., “This account belongs to my ex-spouse”). Future lenders will see this note.

Frequently Asked Questions (FAQ)

Does disputing an error hurt my credit score?

No. Filing a dispute has zero negative impact on your score. In fact, while an account is under dispute, the bureau may temporarily hide the negative marks associated with it, which could temporarily raise your score.

Can I pay a “Credit Repair” company to do this?

You can, but you shouldn’t. Credit repair companies simply send the same letters you can send yourself for the cost of a stamp. They cannot legally remove accurate information, no matter what they promise.

How long does it take to fix a credit report error?

The bureau must resolve the investigation within 30 days (45 days in rare cases). If they decide to remove the error, your score should update the next time your report refreshes, usually within 30 days after the decision.

Why did the error come back after it was deleted?

This is called “re-insertion.” If a creditor later proves the debt is valid, the bureau can put it back on your report. However, they must send you a written notice within 5 days of re-inserting it. If they don’t, you can dispute it again for a procedure violation.