How to Dispute Hard Inquiry on Your Credit Report and Win

Dispute hard inquiry entries on your credit report as soon as you spot them — especially if you didn’t authorize them. Your credit report is a key factor in determining your financial opportunities, whether it’s qualifying for a mortgage, getting a credit card, or even applying for a job. That’s why it can be so frustrating to discover a hard inquiry you didn’t recognize. If this happens, don’t panic you have the right to take action and possibly have it removed from your credit report.

In this guide, we’ll walk you through exactly when to dispute hard inquiry, how to do it (and win), and what to do if your dispute is rejected.

When Should You Dispute Hard Inquiry?

Before jumping into the process, it’s important to understand when you’re eligible to dispute hard inquiry.

You should only dispute hard inquiries that meet one of the following conditions:

- You did not give permission for the inquiry

- The inquiry is the result of identity theft or fraud

- There is a clerical or reporting error by a creditor or bureau

If you did apply for a loan, credit card, apartment rental, or even a car lease and you consented to a credit check that hard inquiry is likely valid and cannot be removed through a dispute. So review your records carefully before taking the next step.

Tip: If you’re unsure about a creditor name, search it online, some lenders operate under unfamiliar legal names.

How to Dispute Hard Inquiry: Online or Mail?

You have two main options when filing your dispute: online or by mail. Each credit bureau allows you to dispute hard inquiry directly with them.

Dispute Hard Inquiry Online (Fastest)

This is the quickest and easiest way to initiate a dispute:

- Experian: https://www.experian.com/disputes

- Equifax: https://www.equifax.com/personal/credit-report-services/credit-dispute/

- TransUnion: https://www.transunion.com/credit-disputes/dispute-your-credit

Just create or log in to your account, select the inquiry in question, and submit your dispute with documentation.

Dispute Hard Inquiry by Mail (More Formal)

If you prefer a paper trail, or want to include physical documents, mail is a solid choice. Send a letter to each bureau using these addresses:

- Equifax

P.O. Box 740256

Atlanta, GA 30374-0256 - Experian

P.O. Box 4500

Allen, TX 75013 - TransUnion

P.O. Box 2000

Chester, PA 19016

We recommend using certified mail with return receipt requested.

What to Include When You Dispute Hard Inquiry

To give your dispute the best chance of success, include the right information and documents. Whether online or by mail, here’s what to prepare:

[Your Full Name]

[Your Address]

[City, State, ZIP Code]

[Phone Number]

[Email Address]

[Date]

Subject: Dispute of Unauthorized Hard Inquiry

To Whom It May Concern,

I am writing to formally dispute hard inquiry listed on my credit report. I did not authorize this credit inquiry and have no relationship with the organization that requested it. The details are as follows:

- Creditor: [Company Name]

- Date of Inquiry: [MM/DD/YYYY]

- Credit Bureau: [Equifax/Experian/TransUnion]

Please investigate and remove this unauthorized inquiry from my credit file. I have enclosed a copy of my credit report highlighting the entry, along with proof of identity and address.

Thank you for your prompt attention.

Sincerely,

[Signature if mailing]

Supporting Documents

Be sure to include:

- A copy of your credit report with the inquiry highlighted

- A government-issued ID (driver’s license, passport)

- A utility bill or bank statement to verify your address

If you suspect identity theft, also include a police report or FTC identity theft affidavit (https://identitytheft.gov).

What Happens After You Dispute Hard Inquiry?

Once the credit bureau receives your dispute, they’re required by law to investigate within 30 days. Here’s what typically happens:

- The bureau contacts the lender or company that placed the inquiry.

- The lender must verify whether you gave permission.

- If they can’t prove authorization, the inquiry will be removed.

- You’ll be notified of the result by mail or online (depending on your submission method).

Possible Outcomes

- Inquiry Removed: If unauthorized or unverifiable, the bureau deletes it from your report.

- Inquiry Verified: If the lender proves it was authorized, it remains on your report.

- No Response: If the lender fails to respond in time, the inquiry may be removed automatically.

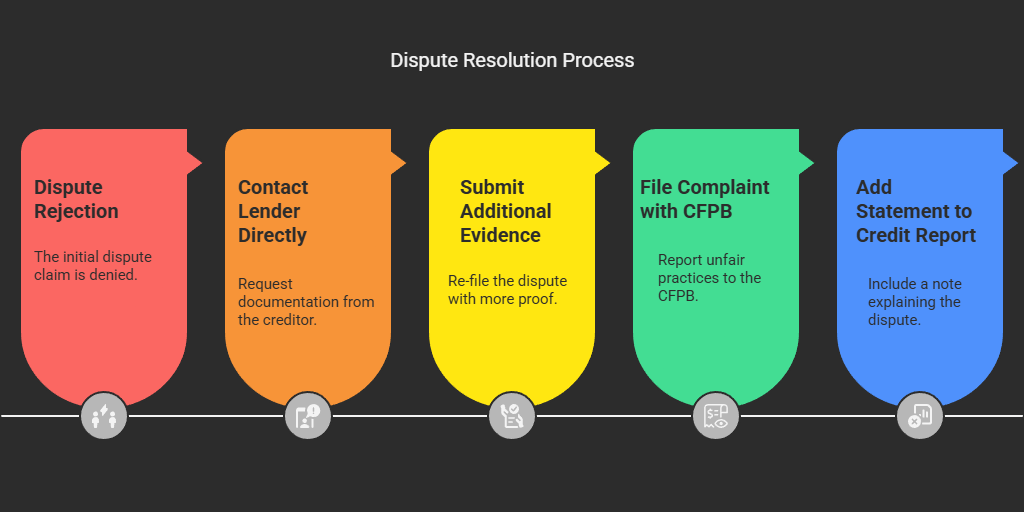

What If Your Dispute Is Rejected?

Even if your dispute hard inquiry claim is denied, don’t give up. You still have options to fight back:

1. Contact the Lender Directly

Ask the creditor to provide documentation showing your consent to the inquiry. If they can’t provide proof, request that they contact the bureau and remove it.

2. Submit Additional Evidence

You can re-file your dispute with extra documentation — like emails, call logs, or legal affidavits if identity theft is involved.

3. File a Complaint with the CFPB

If you believe the bureau or creditor acted unfairly, file a complaint with the Consumer Financial Protection Bureau:

👉 https://www.consumerfinance.gov/complaint/

4. Add a Statement to Your Credit Report

Even if the inquiry stays, you can add a consumer statement to your credit file explaining the dispute for future lenders to see.

Final Thoughts: Stay Proactive About Your Credit

To dispute hard inquiry entries is not just about protecting your credit score — it’s about protecting your identity and your financial integrity. By catching unauthorized inquiries early and acting fast, you can prevent further damage and ensure your report accurately reflects your financial behavior.

Check your credit report regularly (at AnnualCreditReport.com) and don’t be afraid to challenge any entry that looks suspicious. You have the right to dispute hard inquiries, and in many cases, you can win.