How to Get Your Free Credit Report from All 3 Bureaus: Fast and Secure

Why You Need Your Credit Report First

Before applying for any financial product whether it’s a credit card, loan, mortgage, or even renting an apartment your credit report plays a critical role in the decision-making process. It acts as your financial résumé, showing lenders how responsibly you’ve managed credit in the past. That’s why checking your free credit report regularly is one of the smartest things you can do. It not only helps you spot errors or fraudulent activity early but also gives you the confidence and clarity to move forward when seeking better rates, approvals, or even job opportunities that require a background check.

But beyond that, regularly reviewing your credit report empowers you to catch errors, detect fraud, and better manage your credit score. Many people discover identity theft or unauthorized accounts only after reviewing their credit reports. With hard enquiries, for example, a lender may pull your report without your knowledge—and if done fraudulently, it could lower your credit score unnecessarily. That’s why the first step in managing your credit is knowing exactly what’s on your report.

The Role of Credit Reports in Managing Enquiries

Credit enquiries are requests to view your credit report, typically by a lender or creditor. There are two types: soft and hard enquiries. While soft enquiries don’t affect your credit score, hard enquiries do—especially if you have too many in a short span.

Each hard enquiry stays on your credit report for two years. These can slightly lower your credit score and signal to lenders that you may be financially overextended. By regularly checking your credit report, you can monitor these enquiries and dispute any that are unauthorized. This not only helps you protect your score but also gives you peace of mind knowing that no one is accessing your credit information without permission.

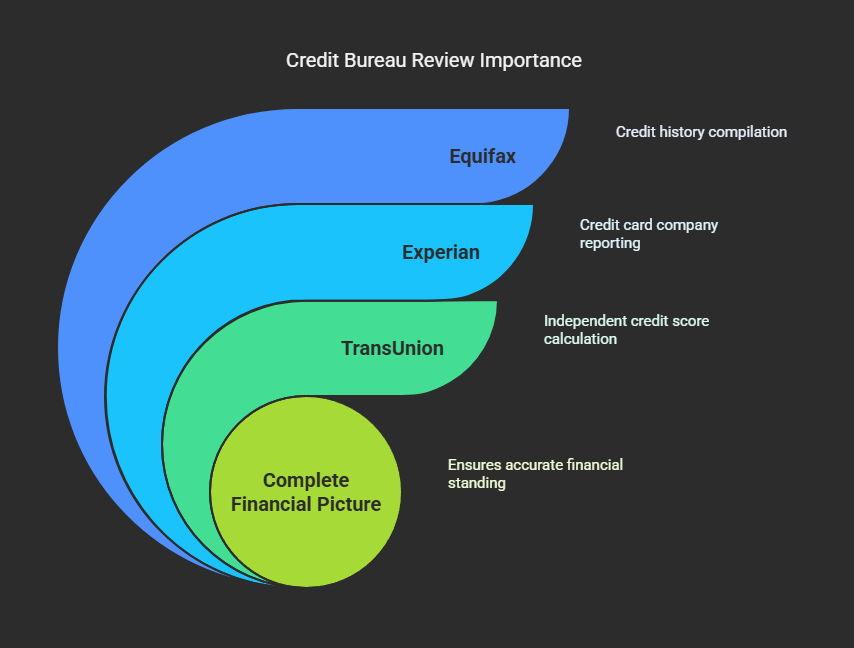

The Importance of Checking All Three Bureaus

In the United States, three major credit bureaus compile your credit history: Equifax, Experian, and TransUnion. Each bureau may have slightly different information depending on the creditors that report to them. That’s why it’s crucial to review reports from all three not just one.

Let’s say your credit card company reports to Experian but not to Equifax. Any updates about that account will only appear in your Experian report. If an error occurs or someone opens an unauthorized account, and it only shows up on TransUnion, you might miss it by only checking one source.

Each bureau independently calculates a credit score based on the data they receive. So, checking all three ensures you get a complete, accurate picture of your financial standing.

Where to Get It

Thankfully, getting your credit report is easier and more secure than ever. Here are the official and reliable sources you should use:

1. AnnualCreditReport.com

This is the only federally authorized website to offer free credit reports from Equifax, Experian, and TransUnion. As of recent updates, you can access your reports weekly for free through this site, a policy extended since the COVID-19 pandemic to help consumers monitor their financial health more actively.

Website: https://www.AnnualCreditReport.com

2. Directly from the Bureaus

Each bureau also allows you to request your report through their websites:

- Equifax: www.equifax.com

- Experian: www.experian.com

- TransUnion: www.transunion.com

They may offer free reports under specific conditions, such as suspected fraud or declined credit.

How Often You Should Check

By law, under the Fair Credit Reporting Act (FCRA), you’re entitled to one free credit report every 12 months from each of the three bureaus. That means you can request one report every four months by rotating between bureaus, helping you stay on top of your credit health year-round.

Best Practices:

- Quarterly Checks: Rotate between bureaus (Equifax in January, Experian in May, TransUnion in September).

- After Major Financial Events: Check after applying for loans, credit cards, or if you’ve been a victim of identity theft.

- Annually at Minimum: If you don’t want to rotate, at least pull all three reports once per year to compare and review.

Some consumers choose to check all three at once, especially before major financial decisions. Others space them out to keep an eye on credit year-round.

What to Look For

Once you have your report, it’s important to know how to read and interpret it. Focus on the following key areas:

1. Personal Information

Ensure your name, address, Social Security number, and employment history are correct.

2. Credit Accounts

Review each account listed—credit cards, loans, mortgages. Check that balances, payment history, and credit limits are accurate.

3. Credit Inquiries

You’ll see a section for recent enquiries. Verify that all hard enquiries were authorized. If you see a lender you don’t recognize, this could be a red flag.

4. Collections and Public Records

If you have any debts in collections or legal judgments, they’ll appear here. Even small medical debts can end up in collections, so keep an eye out.

5. Fraud Alerts or Freezes

Make sure you haven’t unknowingly placed or removed a credit freeze. If you’ve requested a fraud alert, confirm it appears correctly.

Avoiding Fake Credit Report Sites

The internet is full of imposter sites claiming to offer “free credit reports” but are actually looking to sell your data, enroll you in paid subscriptions, or worse—steal your identity. To protect yourself, stick to well-known and officially recognized websites.

Signs of a Legitimate Source:

- Ends in “.gov” or is listed by a government agency (e.g., AnnualCreditReport.com).

- Doesn’t ask for payment for basic report access.

- Uses HTTPS encryption (look for a padlock in the browser).

- Doesn’t require you to enter your credit card number to get a free report.

- Is recommended by the Consumer Financial Protection Bureau (CFPB) or Federal Trade Commission (FTC).

If a site pressures you into purchasing your score or other services, that’s a red flag. You’re entitled to your full report for free, no strings attached.

Final Thoughts: Take Control of Your Credit

Knowing what’s in your credit report is one of the most powerful tools for financial independence. Whether you’re planning a big life event or just want to boost your credit score, starting with a free credit report gives you the clarity you need.

By checking all three credit bureaus regularly and through trusted sources like AnnualCreditReport.com, you stay informed and secure. You’ll catch errors before they hurt your score, monitor for identity theft, and feel more confident when applying for credit.

So don’t wait—get your free reports today. It’s fast. It’s secure. And it’s your right.