How to Spot Unauthorized Hard Inquiries on Your Credit Report — Before They Hurt Your Score

When it comes to your financial well-being, your credit report is more than just a number—it’s your financial reputation. But what if something appears on your report that you didn’t authorize? That’s where unauthorized hard inquiries become a serious concern. These can quietly drag down your credit score, raise red flags to lenders, and even signal identity theft.

If you’ve never heard of unauthorized hard inquiries or aren’t sure how to spot them, this guide is for you. Let’s explore what they are, how they happen, and how to take action before they hurt your financial future.

What Are Unauthorized Hard Inquiries?

To understand unauthorized hard inquiries, you first need to know what a hard inquiry is. A hard inquiry happens when a lender checks your credit report to evaluate your creditworthiness usually when you apply for a credit card, auto loan, mortgage, or similar financial product. These inquiries require your permission.

An unauthorized hard inquiry, on the other hand, is a credit check that shows up on your report without your consent. That’s not just a nuisance, it can be a sign of fraud, a reporting mistake, or an error caused by mistaken identity.

Each hard inquiry may reduce your credit score by a few points, but if you’re not actively applying for credit, any hard inquiry should be questioned immediately.

Hard Inquiry vs. Soft Inquiry: Know the Difference

Before jumping into red flags, it’s important to understand the difference between hard and soft inquiries. Confusing the two could lead to unnecessary worry.

| Type | Impacts Credit Score? | Visible to Lenders? | Common Example |

|---|---|---|---|

| Hard Inquiry | Yes | Yes | Applying for a credit card or loan |

| Soft Inquiry | No | No | Checking your own credit score |

Soft inquiries happen without affecting your score, such as when you check your credit, receive pre-approved offers, or undergo a background check. Only hard inquiries affect your score, and when they appear without your knowledge, they become unauthorized hard inquiries, which require your attention.

Red Flags of Unauthorized Hard Inquiries

Spotting unauthorized hard inquiries is not always straightforward. Many people don’t even notice them until their credit score drops. Here’s what to watch for:

1. Lender Names You Don’t Recognize

If you see an unfamiliar financial institution listed on your report and you haven’t applied for credit recently, investigate immediately. Some lenders operate under different brand names, so do a quick online search to verify them.

2. Suspicious Timing

See an inquiry dated during a time when you weren’t applying for any new credit or financial service? That’s a major warning sign of an unauthorized hard inquiry.

3. Multiple Inquiries in a Short Timeframe

A string of hard inquiries within a short period could be a sign of identity theft. Fraudsters often apply for multiple credit products quickly before getting caught.

4. Repeated Inquiries from the Same Lender

Sometimes, a lender may run multiple credit checks when one would suffice. If you didn’t approve more than one application, it’s worth asking questions.

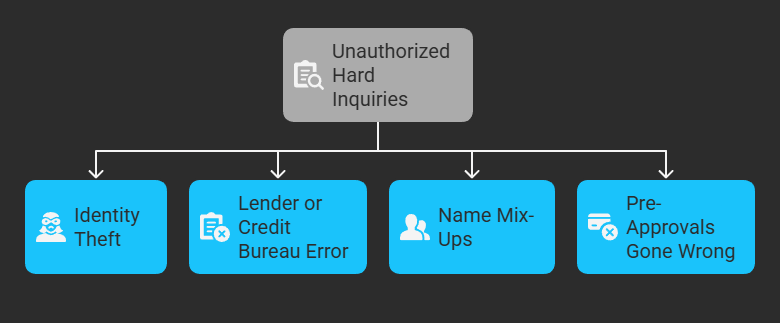

Common Causes of Unauthorized Hard Inquiries

There are a few reasons why unauthorized hard inquiries show up on your report—even if you’ve been careful.

1. Identity Theft

The most serious cause of unauthorized hard inquiries is fraud. If someone has stolen your personal information like your name, Social Security number, or address—they may attempt to open credit accounts in your name.

2. Lender or Credit Bureau Error

Mistakes happen. A lender could have keyed in the wrong information and accidentally pulled your report. Similarly, a credit bureau may have assigned someone else’s inquiry to your report.

3. Name Mix-Ups

If you share a name with a parent, child, or relative (e.g., John Smith Sr. and John Smith Jr.), credit bureaus can sometimes mix up records. This is a common, frustrating reason for unauthorized hard inquiries.

4. Pre-Approvals Gone Wrong

Some companies mistakenly conduct a hard inquiry during a pre-approval process that should have only required a soft pull. Always ask whether a credit pull will be soft or hard before applying.

Why You Must Act Fast Against Unauthorized Hard Inquiries

The sooner you identify and act on an unauthorized hard inquiry, the better. Here’s why speed matters:

- Hard inquiries stay on your report for up to 2 years.

- Too many hard inquiries can label you as a high-risk borrower.

- A lower credit score can impact your ability to qualify for loans, credit cards, or even apartments.

Even a single unauthorized hard inquiry can be the tip of the iceberg—possibly indicating ongoing identity theft or deeper data breaches.

Checklist: Spotting and Investigating Hard Inquiries

Use this simple checklist whenever you review your credit report. If anything looks off, it could be an unauthorized hard inquiry:

| What to Check | Why It Matters |

|---|---|

| ✅ Lender’s Name | Do you recognize the company listed? |

| ✅ Date of Inquiry | Were you applying for credit at that time? |

| ✅ Credit Bureau | Is it reported on Equifax, Experian, or TransUnion? |

| ✅ Type of Inquiry | Is it clearly marked as a hard pull, not soft? |

| ✅ Product Type | Does it match what you applied for (if anything)? |

If one or more of these details don’t make sense, it’s time to investigate.

What to Do If You Find Unauthorized Hard Inquiries

If you confirm an unauthorized hard inquiry on your credit report, here’s a step-by-step plan to remove it and protect your identity:

Step 1: Contact the Lender

Reach out to the company that performed the inquiry. Ask for details, and let them know you didn’t authorize the pull. In many cases, they can withdraw the request or provide more information.

Step 2: File a Dispute with the Credit Bureau

Dispute the inquiry through Experian, Equifax, or TransUnion. Most allow online disputes and typically investigate within 30 days.

Step 3: Report Identity Theft (If Applicable)

If the inquiry is part of broader fraud, visit identitytheft.gov to file a formal identity theft report and begin recovery.

Step 4: Place a Fraud Alert or Freeze

Placing a fraud alert warns lenders to take extra steps before issuing credit in your name. A credit freeze goes further, preventing any new credit from being opened entirely.

Final Thoughts: Stay Ahead of Unauthorized Hard Inquiries

Unauthorized hard inquiries are more than a minor inconvenience—they can be a warning sign of larger issues. The best way to defend your credit is to stay informed, act quickly, and monitor your reports regularly.

You’re entitled to a free credit report every year from each major bureau (Experian, Equifax, and TransUnion) at AnnualCreditReport.com. Use it to stay ahead of any unauthorized activity.

Remember: The earlier you catch an unauthorized hard inquiry, the easier it is to get it removed and the better your chances of protecting your credit score and financial future.