Can You Pay Rent With a Credit Card? The Ultimate Guide to Pros, Cons, and Smart Strategies

Paying rent is one of the largest monthly expenses for most people, often consuming 30–50% of their income. With such a significant outlay, it’s natural to wonder: Can I pay rent with a credit card to earn rewards, improve cash flow, or build credit?

The short answer is yes, but the real question is whether it’s financially wise. This comprehensive guide explores:

- How credit card rent payments work (and the hidden fees)

- The best platforms (including no-fee options like Bilt)

- Impact on credit scores (utilization, payment history, and reporting)

- When it makes sense (and when it’s a dangerous move)

- Smart alternatives (rent reporting, ACH transfers, and more)

By the end, you’ll know exactly whether swiping for rent is a strategic financial move or a costly mistake.

How Paying Rent With a Credit Card Works

Most landlords and property management companies don’t accept credit cards directly due to high processing fees (typically 2–4% per transaction). However, third-party services act as intermediaries:

- You pay the platform via credit card (online or through an app).

- The platform sends funds to your landlord via check, ACH, or direct deposit.

- You incur fees (usually 2.9–3.5%) unless using a no-fee option like Bilt.

Example of Fees vs. Rewards

Let’s say your rent is $1,500/month, and your credit card offers 2% cash back:

- Processing fee (3%): $45/month ($540/year)

- Cash back (2%): $30/month ($360/year)

- Net loss: $15/month ($180/year)

Unless you’re using a no-fee card or meeting a sign-up bonus, the math rarely works in your favor.

Best Platforms to Pay Rent With a Credit Card

1. Bilt World Elite Mastercard® (Best for No Fees & Rewards)

- No processing fees on rent payments (if using the Bilt app).

- Earn 1x points per $1 on rent (up to 100,000 points/year).

- Bonus rewards: 3x on dining, 2x on travel, 5x on Lyft.

- Unique feature: Bilt mails a check to your landlord if they don’t accept digital payments.

Ideal for: Renters who want to earn rewards without fees.

2. Plastiq (Best for Flexibility)

- Fee: 2.9% per transaction.

- Works with any landlord (sends a check or ACH).

- Useful for: One-time payments or meeting credit card sign-up bonuses.

3. PlacePay (Best for Roommates)

- Fee: 2.99% for credit cards, $1.95 for ACH.

- Supports rent-splitting among multiple tenants.

- Auto-pay and mobile app for convenience.

4. PayPal & Venmo (Limited Use Cases)

- Some landlords accept these, but fees apply (~3%).

- Risk: May code as a “cash advance” (higher APR, no rewards).

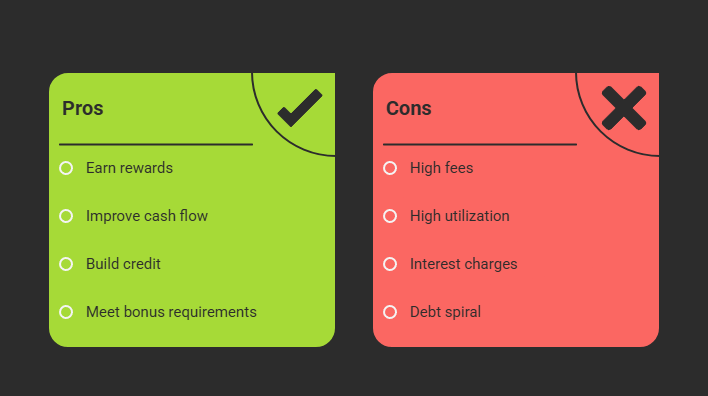

Pros of Paying Rent With a Credit Card

Earn Rewards on a Major Expense

- If your card offers 2–5% cash back or travel points, you can turn rent into free flights, statement credits, or even future rent payments (e.g., Bilt’s rewards).

Improve Cash Flow Temporarily

- If rent is due before payday, charging it buys you 20–30 days until the credit card bill is due (just pay in full to avoid interest).

Build Credit History (Indirectly)

- While rent payments aren’t automatically reported to credit bureaus, using a credit card responsibly (low utilization, on-time payments) helps your score.

Meet Sign-Up Bonus Requirements

- Many premium cards (e.g., Chase Sapphire Preferred) require $3,000–$5,000 in spending in 3 months. Charging rent can help hit that threshold.

Cons of Paying Rent With a Credit Card

High Processing Fees (2.9–3.5%)

- On a $1,500 rent payment, a 3% fee = $45/month or $540/year—often more than the rewards earned.

Risk of High Credit Utilization

- If your credit limit is $5,000 and you charge $1,500 in rent, your utilization jumps to 30% (ideally, keep it below 10% for the best credit score).

Interest Charges If You Carry a Balance

- Credit card APRs average 20–30%. If you can’t pay the full balance, interest quickly outweighs rewards.

Potential for Debt Spiral

- Using credit to cover rent can mask budget issues and lead to long-term debt.

How Paying Rent With a Credit Card Affects Your Credit Score

Using pay rent with a credit card doesn’t just impact your bank account—it can also influence your credit score in several important ways. Understanding the three main credit factors affected can help you make smarter financial decisions and avoid unnecessary harm to your credit profile.

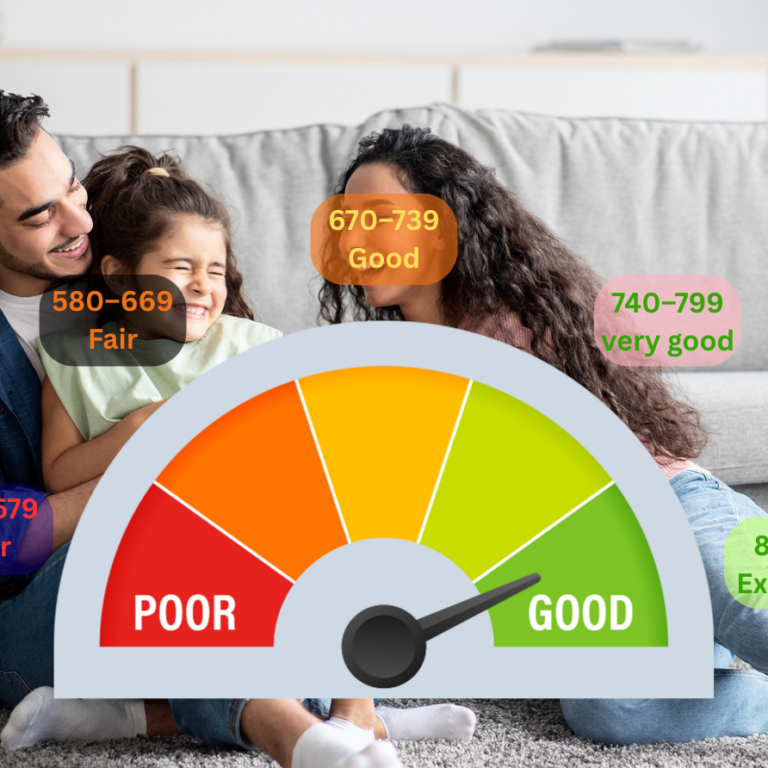

1. Credit Utilization Ratio (30% of Your Score)

Your credit utilization ratio is the amount of revolving credit you’re using compared to your total credit limit. This is one of the most significant factors in your FICO credit score.

Example:

- Credit limit: $4,000

- Rent charged: $1,200

- Utilization rate: 30%

At 30% utilization, you’re right at the threshold where lenders begin to view you as a higher risk. Ideally, you should aim to keep your utilization under 10% for the best credit score impact.

Why it matters: High utilization, even for just a short time, can temporarily lower your credit score by 20 to 50 points or more. This can affect your ability to qualify for loans, new credit cards, or even housing.

Fixes and Best Practices:

- Request a credit limit increase to spread the same spending over a higher limit, lowering the utilization percentage.

- Pay down your balance early (before your statement closing date) to reduce the reported utilization.

- Use multiple cards and split payments to keep each card’s utilization low.

2. Payment History (35% of Your Score)

Your payment history is the single most important factor in your credit score. Paying rent with a credit card won’t help your score unless you pay your credit card bill on time—every month.

What can go wrong:

- If you’re late on your credit card payment, even by just one day, your credit score could drop 50 to 100 points, depending on your history and other accounts.

- Missed payments stay on your credit report for up to seven years, even if you eventually catch up.

Best Practice:

- Set up autopay for at least the minimum payment to avoid late fees and negative marks.

- If your budget is tight, don’t charge more than you can repay within the same billing cycle.

3. Rent Reporting to Credit Bureaus

Typically, rent payments aren’t included in your credit report unless your landlord or payment platform reports them. This is where services like AxcessRent and Bilt Rewards come in.

- Bilt Mastercard reports rent payments as part of your revolving credit account, helping you build a history of on-time payments.

- AxcessRent enables tenants to build credit by reporting monthly rent payments directly to major credit bureaus like Equifax and TransUnion.

Why it matters:

- This positive reporting can boost your credit profile, especially for renters who have little or no credit history (students, young adults, new immigrants).

- Rent reporting helps turn your largest monthly expense into an asset for your credit journey, without taking on new debt.

When Should You Pay Rent With a Credit Card?

Paying rent with a credit card can offer flexibility and rewards—but it’s not always the smartest financial move. To help you decide, here’s a breakdown of when it’s a smart strategy and when it could backfire.

Good Scenarios to Use a Credit Card for Rent

Paying rent with a credit card can be beneficial in the following situations:

1. Using a No-Fee Credit Card Like Bilt

Cards like the Bilt World Elite Mastercard® allow you to pay rent with a credit card without any processing fees and still earn rewards—something most cards don’t offer.

- Earn points on rent (up to 100,000 points per year)

- Build credit with every rent payment

- Use points for travel, fitness, decor, or even a home down payment

💡 Pro tip: You can even pay landlords who don’t accept cards directly—Bilt will mail them a check on your behalf.

2. Meeting a Credit Card Sign-Up Bonus

Many premium rewards cards offer large welcome bonuses for spending a set amount in a short period.

Example:

- Requirement: Spend $4,000 in 3 months

- Reward: Get 80,000 bonus points (worth $800–$1,200)

Charging your rent to your card can help you meet that goal faster—especially if your rent is $1,200+ per month.

3. Short-Term Cash Flow Issues (But You Can Repay Quickly)

Life happens. If your rent is due before payday, using a credit card can give you some breathing room—as long as you can pay off the full balance within the billing cycle.

- Avoid late fees from your landlord

- Stay current on rent without borrowing from friends or family

- Maintain your payment history for credit score health

🚨 Just don’t make this a habit, or it could snowball into debt.

When Paying Rent With a Credit Card Is a Bad Idea

Sometimes, pay rent with a credit card can hurt more than it helps. Here are situations where you should avoid it:

1. You Carry a Balance Month-to-Month

Credit cards often have APRs above 20%, which can erase any rewards you earn—and then some.

Example:

- Rent = $1,200

- APR = 24%

- Interest after 6 months = ~$150+

If you can’t pay off your balance in full, you’re essentially taking a high-interest loan just to pay rent with a credit card. Not worth it.

2. Your Credit Limit Is Low

Let’s say you have a $2,000 limit and pay $1,200 rent—that’s 60% utilization, which can severely hurt your credit score.

High utilization signals to lenders that you may be overextended financially.

🔧 Fix: Ask for a credit limit increase or use multiple cards to split the payment (if fees are manageable).

3. You’re Already in Credit Card Debt

Adding another large charge to your card only worsens your debt-to-income ratio and can trap you deeper in interest payments.

If you’re already struggling with minimum payments, it’s smarter to explore:

- Emergency rent assistance programs

- Short-term loans with lower APRs

- Talking to your landlord about a payment plan

Smart Alternatives to pay rent with a credit card

1. ACH/Bank Transfers (Usually Free)

- Most landlords offer fee-free ACH payments.

2. Rent Reporting Services (Build Credit Without a Card)

- AxcessRent: Reports rent payments to credit bureaus without needing a credit card.

- Bilt Rewards: Even if you don’t use their card, they report rent payments.

3. Emergency Fund (Avoid Reliance on Credit)

- Save 1–2 months’ rent in a high-yield savings account for flexibility.

Final Thoughts: Credit Card Rent Payments — Smart or Risky?

Pay rent with a credit card can be a smart financial move—if done responsibly. It offers short-term flexibility, helps meet credit card sign-up bonuses, and when paired with platforms like AxcessRent or Bilt, it can even help you build credit through on-time rent reporting. If you’re financially disciplined, pay your balance in full every month, and use a card with no or low processing fees, this method can maximize rewards and enhance your credit profile over time.

However, the risks are real. High interest rates, processing fees (often 2.5%–3%), and increased credit utilization can hurt your credit score and lead to long-term debt if not managed carefully. If you’re already struggling with credit card debt or your income isn’t consistent, pay rent with credit card this way may do more harm than good. Always assess your financial habits, know your limits, and choose the method that aligns with your goals. Smart use creates opportunity—careless use invites consequences.

Frequently Asked Questions (FAQ)

Can I pay rent with a credit card if my landlord doesn’t accept cards?

Yes. Services like Plastiq and Bilt can process your credit card payment and send a check or ACH to your landlord on your behalf.

Does paying rent with a credit card hurt your credit?

It can hurt if you carry a balance or max out your limit. But if you pay in full and keep utilization low, it can help by adding payment history.

Is there a credit card with no rent processing fees?

Yes! The Bilt Mastercard allows rent payments with no fee, as long as you use the Bilt app.