Placing or Lifting a Credit Freeze: What You Should Know

When it comes to protecting your financial identity, few tools are as powerful and effective as a credit freeze. Whether you’re concerned about identity theft, have been a victim of a data breach, or simply want to prevent unauthorized access to your credit, freezing your credit report is a smart and proactive step. This comprehensive guide walks you through what a credit freeze is, how it works, and exactly how to place or lift one with ease.

What Is a Credit Freeze?

A credit freeze, also known as a security freeze is a tool that allows you to restrict access to your credit report. When frozen, credit bureaus prevent lenders, creditors, and other third parties from pulling your credit file for the purpose of opening new accounts. This means if a scammer tries to apply for a credit card, auto loan, or even a mortgage in your name, they’ll be stopped in their tracks.

It’s important to note that a credit freeze does not impact your current accounts. You can still use your existing credit cards, repay loans, and check your own credit report while it’s frozen. The freeze is specifically designed to block new credit activity unless you give permission.

Why Would Someone Want to Freeze Their Credit?

Freezing your credit isn’t just for people who have already been victims of identity theft—though it’s especially important for them. There are several compelling reasons why you might consider freezing your credit:

- Data Breaches Are Common: Millions of Americans have had their personal data compromised through breaches at major companies, healthcare providers, and even government agencies. A credit freeze ensures that stolen data can’t easily be used to open new accounts.

- No Immediate Need for New Credit: If you’re not planning to apply for a loan or credit card soon, freezing your credit adds an extra layer of protection without disrupting your daily finances.

- Peace of Mind: Even if no fraud has occurred, knowing that no one—not even you—can open a new account unless you unfreeze your credit gives you confidence that your identity is secure.

Does a Credit Freeze Affect Your Credit Score?

No. Freezing your credit has zero impact on your credit score. It doesn’t affect your ability to use current accounts, nor does it change your payment history or credit utilization—two of the most important factors that influence your score.

Additionally, a freeze does not appear on your credit report. Lenders won’t even know you have one in place unless they attempt to access your report and are blocked from doing so.

What’s the Difference Between a Credit Freeze and a Fraud Alert?

While both a credit freeze and a fraud alert are tools designed to protect your credit, they function differently:

- A fraud alert tells lenders to take extra precautions before extending credit, such as contacting you directly for confirmation. It doesn’t block access to your credit file, but it makes fraud more difficult.

- A credit freeze, on the other hand, stops all new credit inquiries in their tracks unless you explicitly lift it.

If you’ve already been targeted by identity thieves, it’s a good idea to use both. You can start with a fraud alert (which is easier to manage), and if threats persist, upgrade to a full credit freeze for tighter security.

How Do You Place a Credit Freeze?

Placing a credit freeze is a simple, free process—but you must do it individually at all three major credit bureaus:

Equifax

- Website: https://www.equifax.com/personal/credit-report-services/credit-freeze/

- Phone: 1-800-349-9960

Experian

- Website: https://www.experian.com/help/credit-freeze/

- Phone: 1‑888‑397‑3742

TransUnion

- Website: https://www.transunion.com/credit-freeze

- Phone: 1-888-909-8872

What You’ll Need:

To place a freeze, you’ll be asked to provide personal details to verify your identity:

- Full legal name

- Social Security number

- Date of birth

- Current and past addresses

- A copy of a government-issued photo ID (e.g., driver’s license or passport)

- A utility bill, bank statement, or insurance document showing your current address

Once your request is processed, each bureau will issue you a PIN or login credentials. Keep these secure—you’ll need them to lift the freeze later.

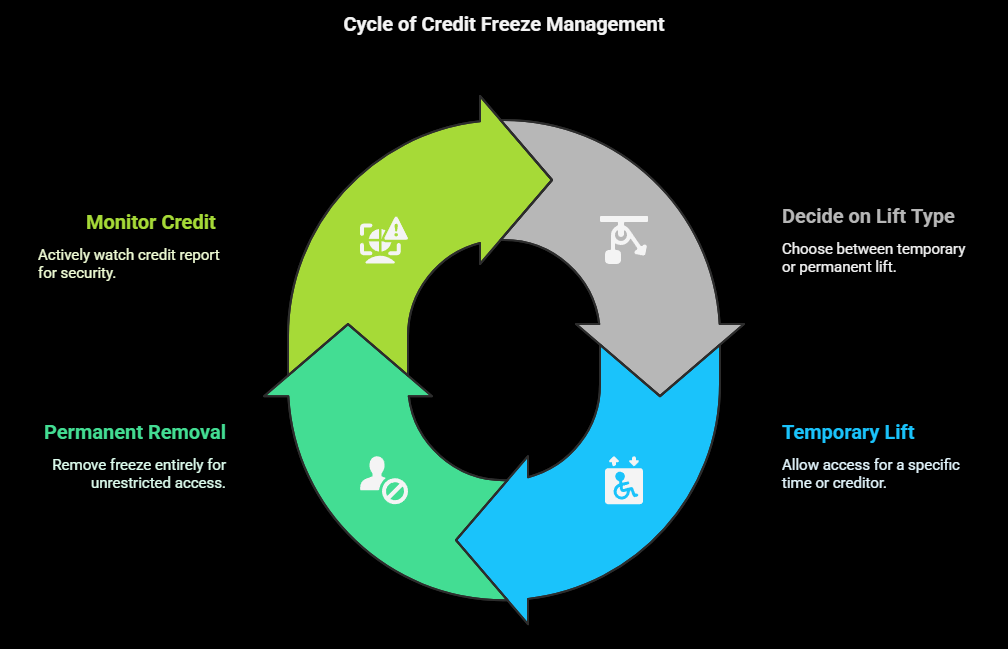

How Do You Lift or Temporarily Thaw a Credit Freeze?

Lifting a credit freeze, whether temporarily or permanently—is a simple but secure process that puts control of your credit file back in your hands when you need it. There are two primary ways to lift the freeze, and the right option depends on your situation:

1. Temporary Lift

If you’re applying for a loan, mortgage, or credit card, you can temporarily lift your freeze for a specific time window or for a specific creditor. This allows them to access your report while keeping it secure from others.

Ensures that your credit report is only accessible for a limited time or to a limited party, keeping it protected from everyone else. It’s a great balance between security and convenience—especially if you want to re-freeze your credit automatically afterward.

2. Permanent Removal

If you’re done with the freeze altogether and no longer want your credit restricted, you can request a permanent lift. This option is suitable if:

- You’re planning to apply for multiple lines of credit in the near future

- You’re managing your credit actively and don’t feel at risk of identity theft

- You find it more practical to monitor your report than freeze it

Once permanently removed, your credit file will remain open to lenders until you decide to freeze it again.

How to Manage Freezes at the Credit Bureaus

Each of the three major credit bureaus—Equifax, Experian, and TransUnion—provides online tools, mobile apps, and phone support to help you manage your freeze. You’ll need to authenticate your identity using the PIN, password, or credentials you received when you first placed the freeze.

Here’s a quick breakdown of your options:

- Online: The fastest and easiest method. Simply log into your account, select the freeze management option, and choose either temporary or permanent lift.

- Phone: Call the credit bureau’s toll-free line and follow the prompts. You’ll still need your PIN or credentials.

- Mail: If you prefer paper, you can submit a written request, but this method takes longer—up to three business days after receipt.

How Long Does It Take to Unfreeze Credit?

Federal law requires the credit bureaus to lift a freeze within one hour if the request is made online or by phone. If you request it by mail, they must act within three business days of receiving your documents.

For most users, lifting the freeze online is quick, often taking just a few minutes.

What If I Lose My PIN or Password?

If you lose your PIN or credentials, each credit bureau has a secure recovery process. You’ll need to verify your identity again—usually by submitting a copy of your ID and a recent bill.

Pro tip: Store your freeze credentials in a password manager or secure physical file. It’s critical to access them quickly if you need to lift the freeze in a hurry.

Can Employers, Landlords, or Insurance Companies See My Credit When Frozen?

Yes—but with some limitations. A credit freeze primarily restricts new credit activity by blocking most lenders and creditors from accessing your credit report. However, it does not completely lock down your credit file from all types of access. Certain parties and situations are exempt from the freeze under federal law.

- Current creditors (e.g., your bank or credit card issuer)

- Debt collectors acting on behalf of those creditors

- Government agencies with legal authority (e.g., court orders or tax matters)

- Employers or landlords, but only if you give written permission

A freeze mainly blocks new credit applications—not other valid or ongoing uses of your credit report.

Does Freezing Credit Block Soft Inquiries?

No, placing a credit freeze does not block soft inquiries, also known as soft pulls. While a freeze restricts access to your credit report for most new credit applications, it does not prevent all types of credit-related activity. Soft inquiries are considered low-risk and do not require your permission, so they remain unaffected by a freeze.

Soft inquiries can include:

- Checking your own credit report or score: You can still access your credit file through services like Credit Karma, Experian, or directly from the credit bureaus without lifting the freeze. Monitoring your credit is encouraged—even while it’s frozen.

- Pre-approved credit card or loan offers: Lenders often conduct soft inquiries to determine if you qualify for promotional offers. These offers may still appear in your mailbox or inbox, even when your credit is frozen.

- Promotional or account review inquiries: Companies you already have financial relationships with—like your credit card issuer or mortgage lender—may review your credit regularly to assess account risk or offer new services.

- Credit monitoring services: If you’re using tools to keep track of your score or receive alerts, those services will still function normally while your credit is frozen.

The key difference is that soft inquiries don’t impact your credit score and are not visible to potential lenders or creditors reviewing your file. They are only visible to you and serve as an internal record of activity.

In contrast, hard inquiries—which happen when you apply for new credit—are blocked when your credit is frozen. These are the types of inquiries that can affect your score and potentially open the door to fraud, which is why freezing your credit is such a powerful protective measure.

So, while a credit freeze limits risky access, it still allows safe, necessary activity to continue in the background—keeping you in the loop without compromising your security.

Should I Freeze My Credit With All Three Bureaus?

Absolutely. Placing a freeze with just one or two bureaus leaves you vulnerable. A determined fraudster only needs access to one unlocked report to open a fraudulent account. Always freeze your credit at:

- Equifax

- Experian

- TransUnion

This ensures maximum protection across all reporting platforms.

Does It Cost Anything to Freeze or Unfreeze Credit?

No. Thanks to the Economic Growth, Regulatory Relief, and Consumer Protection Act of 2018, freezing and unfreezing your credit is completely free for all U.S. consumers. There are no hidden fees, regardless of how many times you lift or reapply the freeze.

Final Thoughts

A credit freeze is one of the most effective tools available for protecting your financial identity in today’s digital world. With data breaches, phishing scams, and synthetic identity fraud on the rise, every adult—and every child—should strongly consider placing a freeze on their credit reports. It’s a free, easy, and reliable way to put yourself in control of your credit profile.

While managing a freeze may take a few extra steps when you’re applying for new credit, the peace of mind it brings is well worth it. You’ll be able to prevent unauthorized access while still using your existing credit cards, repaying loans, and checking your score. Whether you’re taking preventive action or responding to suspicious activity, placing or lifting a credit freeze is a smart financial move that puts your security first.