What Credit Score Is Needed to Buy House?

Buying a home is one of life’s biggest milestones—but also one of its most complex. From picking the right neighborhood to navigating closing costs and interest rates, there’s a lot to consider. However, one thing impacts nearly every step of the mortgage process: your credit score. Whether you’re a first-time homebuyer or upgrading to a bigger place, your credit score can determine whether you get approved for a loan, how much house you can afford, and what kind of interest rate you’ll be offered. And with housing prices rising, even a small difference in your interest rate could cost or save you tens of thousands of dollars over the life of a loan.

So, what credit score do you actually need to buy a house? Is there a minimum score? What happens if your score isn’t high enough right now? This guide answers all your questions in a clear, simple way—so you can confidently take the next step toward homeownership.

So, what credit score is needed to buy house? Let’s break it down.

What’s the minimum credit score needed to buy house?

There isn’t one universal score that works for all mortgage types—it varies depending on the type of loan you’re applying for and the lender’s requirements. But here’s a general breakdown:

- Conventional loans (most common): Minimum score is typically 620

- FHA loans (for lower-income or first-time buyers): As low as 500, but you’ll need 580+ to qualify for a 3.5% down payment

- VA loans (for veterans and active-duty service members): No official minimum, but most lenders prefer 620+

- USDA loans (for rural housing): Typically require 640 or higher

| Conventional Loans | 620 | Most common type; often preferred by lenders |

| FHA Loans | 500 | 580+ needed for 3.5% down payment |

| VA Loans | No official minimum | Typically 620+ preferred by lenders |

| USDA Loans | 640 | For rural area buyers |

These scores are based on standard lender guidelines, but some may vary depending on your financial profile and the lender’s policies.

What’s considered a “good” credit score for buying a home?

While the minimum scores help you get in the door, a “good” credit score will unlock better rates and terms. Based on the VantageScore 3.0 model:

- 661–780 is considered good

- 781–850 is excellent

Higher credit scores show lenders that you’re financially responsible. The better your score, the lower your mortgage interest rate—which means smaller monthly payments and big savings over time.

Why does your credit score matter so much to mortgage lenders?

Your credit score is like a snapshot of your financial trustworthiness. Mortgage lenders use it to decide whether you’ll repay your loan on time—and how much risk they’re taking by lending to you. A higher score tells them:

- You consistently pay your bills on time

- You’re using your credit responsibly

- You’re less likely to default on a loan

That’s why your credit score directly impacts:

- Approval odds

- Interest rates

- Down payment requirements

- Loan size and type

Can you still get a mortgage with a low credit score?

Yes, it’s possible—but it’s not always easy. With a credit score below 620, you may still qualify for an FHA loan, which is backed by the government and designed to help borrowers with limited credit. However, keep in mind:

- You may need a larger down payment

- You’ll likely get a higher interest rate

- Some lenders may still say no

That’s why improving your credit—even a little—before applying can make a big difference.

How can you improve your credit score before applying for a mortgage?

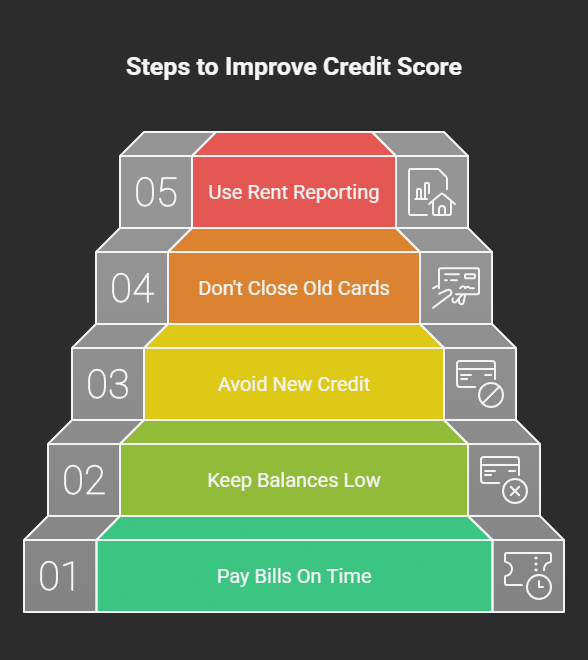

If your credit score isn’t where you want it to be yet, don’t panic. Here are the most effective ways to raise your score in the months before you apply for a home loan:

- Always pay bills on time – Payment history makes up 35% of your score

- Keep credit card balances low – Aim to use less than 30% of your limit

- Avoid new credit applications – Too many hard inquiries can drop your score

- Don’t close old credit cards – They help with the length of your credit history

- Use rent reporting – Platforms like AxcessRent let your rent payments boost your credit

With a few months of smart habits, you can potentially increase your score enough to qualify for better loans and interest rates.

Do all lenders use the same score to evaluate you?

Not exactly. There are multiple scoring models, and each lender might use a different one. Most mortgage lenders use specific versions of the FICO Score, such as:

- FICO Score 2, 4, or 5 (older models)

- Some may use FICO 8 or VantageScore 3.0 for pre-qualification

That’s why your credit score in one app may be slightly different from what your lender sees.

What else do lenders consider besides your credit score?

Your score is important, but it’s not the only factor. Lenders will also look at:

- Your income and employment history

- Debt-to-income (DTI) ratio

- Down payment amount

- Savings and other assets

Even with a great score, you’ll need to show that you can afford your monthly payments.

What if your credit score isn’t high enough right now?

Don’t give up! Many future homeowners start with low credit. You still have options:

- Work on improving your score for a few months

- Use rent reporting tools like AxcessRent to speed up credit building

- Speak to a mortgage advisor—some lenders offer flexible programs

Patience and preparation can make all the difference.

Final Thoughts: Be Credit-Ready for Homeownership

A good credit score isn’t just a number—it’s a key to unlocking lower interest rates, better loan terms, and more home options. While it’s possible to buy a home with less-than-perfect credit, a higher score gives you more control, more savings, and a smoother buying experience.

So if homeownership is on your radar, take time to check your credit, clean up any issues, and strengthen your financial profile. And if you’re already paying rent? Use that to your advantage with rent reporting—services like AxcessRent help turn your rent into credit-building power.

Your dream home may be closer than you think—all it takes is the right plan.