What Is a Credit Builder Loan? A Complete Guide to Building Credit from Scratch

When it comes to building credit, starting from scratch or recovering from past mistakes can feel overwhelming. Traditional credit cards and loans often require a strong credit history—but how do you build credit when you don’t have any? That’s where a Credit Builder Loan comes in.

Unlike typical loans, a credit builder loan is designed specifically to help you build or rebuild your credit score. It’s a simple, low-risk way to establish a credit history while saving money over time. Whether you’re new to credit, recovering from past financial struggles, or simply trying to improve your score, this type of loan can be a smart and strategic tool to get started.

Let’s break down everything you need to know about credit builder loans—how they work, where to get one, the pros and cons, and whether it’s the right option for your financial journey.

What Is a Credit Builder Loan?

A credit builder loan is a type of installment loan specifically designed to help people with little or no credit history begin building one. Instead of giving you the money upfront like a traditional loan, the lender places your loan amount into a secured savings account or certificate of deposit (CD). You make fixed monthly payments (including interest and possibly fees), and once the loan is fully repaid, you get access to the total amount you “borrowed.”

This way, you’re building a positive payment history, one of the biggest factors in your credit score—without the risk of overspending or going into debt.

How Does a Credit Builder Loan Work?

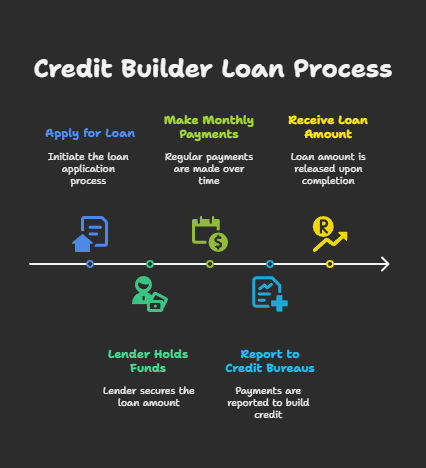

Here’s how a credit builder loan typically functions:

- You apply for a loan—usually for an amount between $300 and $3,000.

- You don’t receive the money right away. Instead, the lender holds it in a secured account.

- You make monthly payments (including principal and interest) over a fixed term—usually between 6 to 24 months.

- Your payments are reported to the credit bureaus, helping to build your credit history.

- Once the loan is paid off, you receive the total loan amount from the secured account.

In essence, it’s a “forced savings” plan that boosts your credit score—if you make all your payments on time.

What Are the Benefits of a Credit Builder Loan?

A credit builder loan offers several unique benefits that make it an ideal option for people new to credit or trying to recover from poor credit:

- Build or repair your credit with consistent, on-time payments.

- Improve your credit mix—adding an installment loan can diversify your credit profile.

- Create a savings cushion—when the loan ends, you get a lump sum of money.

- No prior credit history required—perfect for students, young adults, and those new to the U.S. financial system.

- Helps establish good financial habits by encouraging regular payments.

Where Can You Get a Credit Builder Loan?

There are several places to get a credit builder loan. Some are traditional, while others are digital-first and built for convenience:

- Local banks and credit unions: Many community banks and credit unions offer credit builder loans to help members establish credit.

- Online lenders: Several fintech platforms specialize in credit-building tools and offer fast applications.

- Nonprofit lenders: Some nonprofits and community development financial institutions (CDFIs) offer these loans with flexible terms.

Before choosing a lender:

- Compare interest rates and fees

- Check if they report to all three major credit bureaus (Equifax, Experian, TransUnion)

- Understand the repayment terms and penalties

Typical Terms of a Credit Builder Loan

| Feature | Typical Range |

|---|---|

| Loan Amount | $300 – $3,000 |

| Loan Term | 6 – 24 months |

| Interest Rate | 5% – 16% APR (varies widely) |

| Monthly Payments | Fixed, based on loan size |

| Access to Funds | After final payment |

Some lenders might offer slightly higher or lower limits. Choose a term and payment amount that fits comfortably within your monthly budget.

Are There Any Downsides?

While credit builder loans are a great option for many, it’s important to weigh the potential drawbacks:

- No immediate access to funds—unlike regular loans, you don’t get money upfront.

- Interest and fees apply—you may pay more than what you receive at the end.

- Missed payments hurt your credit—just like any loan, failing to pay on time can damage your score.

- Limited loan amounts—these loans won’t help in emergencies or large purchases.

Who Should Consider a Credit Builder Loan?

This type of loan is a good option for you if:

- You have no credit history or a low credit score.

- You want to establish a solid payment history.

- You need a structured savings plan.

- You’re not yet eligible for other credit options, like unsecured credit cards.

If you’re looking for a secure, structured way to build financial credibility, a credit builder loan is one of the most effective starting points.

Tips for Making the Most of a Credit Builder Loan

To get the most benefit out of your credit builder loan:

- Set up automatic payments to avoid missing due dates

- Choose a realistic loan term and amount that won’t strain your budget

- Monitor your credit score monthly to track progress

- Avoid taking on other debts during the repayment period

- Use rent reporting tools like AxcessRent to boost your score even faster

Final Thoughts: Is a Credit Builder Loan Right for You?

A credit builder loan can be a powerful tool to kickstart or rebuild your credit journey. Unlike most loans, its primary goal is not to help you spend, but to help you save and build credit at the same time. For many, it’s a safe and affordable stepping stone to larger financial goals—like qualifying for a car loan, credit card, or even a mortgage down the road.

Whether you’re just starting your financial journey or recovering from setbacks, smart habits like on-time payments, low utilization, and tools like credit builder loans and rent reporting can help you grow your credit profile with confidence.