What Is a Good Credit Score? A Complete Guide to Understanding and Improving Your Credit

When it comes to your financial well-being, few numbers carry as much weight as your credit score. Whether you’re applying for a mortgage, financing a car, or just trying to get approved for a credit card, lenders use this number to decide how trustworthy you are as a borrower. But what exactly counts as a good credit score—and why does it matter so much?

In this guide, we’ll break down what a good credit score looks like, how it’s calculated, what factors affect it, and—most importantly—how you can build and maintain a strong score for long-term financial success.

What Is a Good Credit Score?

A good credit score typically falls within the range of 661 to 780 based on the VantageScore® 3.0 model. This score range suggests that you’re managing your credit well and are considered a low-risk borrower by most lenders.

| Credit Score Range | Credit Level |

|---|---|

| 300–600 | Poor |

| 601–660 | Fair |

| 661–780 | Good |

| 781–850 | Excellent |

While these ranges vary slightly depending on the scoring model used (like FICO or VantageScore), the key takeaway is this: the higher your score, the more trustworthy you appear to potential lenders—and the more likely you are to get approved with better terms.

Why Does Having a Good Credit Score Matter?

A good credit score is more than just a number—it’s a powerful financial asset that opens doors to better opportunities and savings. Lenders, landlords, and even employers often use it to gauge your financial responsibility. Here’s why maintaining a strong credit score is crucial:

1. Qualify for Better Interest Rates on Loans and Credit Cards

A high credit score signals to lenders that you’re a low-risk borrower, making them more willing to offer you lower interest rates. Whether you’re applying for a mortgage, auto loan, or credit card, even a slightly lower rate can save you thousands over time.

2. Get Approved for Higher Credit Limits

With a good credit score, lenders are more likely to approve you for larger credit limits. This not only gives you greater financial flexibility but can also improve your credit utilization ratio—a key factor in your score—as long as you manage it responsibly.

3. Pay Less Over Time Due to Reduced Interest Costs

Lower interest rates mean you’ll pay less in finance charges over the life of a loan. For example, on a 30-year mortgage, a difference of just 1% in interest could save you tens of thousands of dollars.

4. Improve Your Chances of Renting a Home or Getting Utilities Set Up Easily

Landlords and utility companies often check credit scores to assess reliability. A good score can help you secure your dream apartment, avoid hefty security deposits, and even get approved for services like internet and electricity without extra hurdles.

5. Pass Employment Background Checks (Where Legal)

Some employers, especially in finance or government roles, review credit reports as part of their hiring process (where permitted by law). A strong credit history can reflect positively on your trustworthiness and responsibility.

Over time, the benefits of a good credit score compound, potentially saving you thousands—or even tens of thousands—of dollars compared to someone with poor credit. Whether it’s securing a low-rate mortgage, avoiding high-interest debt, or simply having more financial freedom, a strong credit score is an investment in your future.

What Factors Affect Your Credit Score?

Your credit score is calculated using several components. The two most common models, FICO and VantageScore, use similar factors, including:

- Payment History (35%)

– Are you paying your bills on time? - Credit Utilization (30%)

– How much of your credit are you using compared to your total limit? - Length of Credit History (15%)

– How long have your accounts been open? - Credit Mix (10%)

– Do you have a mix of credit types (loans, cards, retail accounts)? - New Credit Inquiries (10%)

– How often are you applying for new credit?

Maintaining healthy habits in these areas is essential for keeping your score in the “good” or even “excellent” range.

Can Your Credit Score Change Over Time?

Absolutely. Your credit score is a dynamic number that can change frequently depending on the activity on your credit report. Here are some reasons your score might go up or down:

- A missed or late payment

- Increased credit card balances

- Paying down debt

- Opening or closing credit accounts

- Errors or outdated information in your report

- New hard inquiries from credit applications

That’s why it’s important to monitor your credit regularly—and dispute any incorrect information.

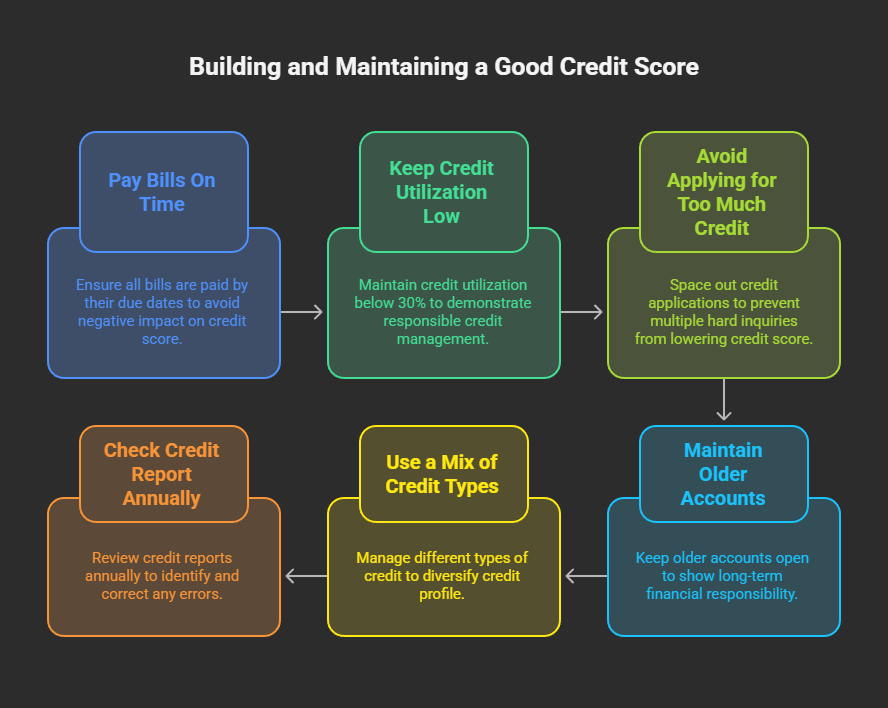

How to Build and Maintain a Good Credit Score

Your credit score plays a crucial role in your financial life, affecting everything from loan approvals to interest rates and even rental applications. If your score isn’t quite where you want it to be, don’t worry—improving it is entirely possible with discipline and the right strategies. Here are some proven tips to help you build and maintain a strong credit score over time:

1. Always Pay On Time

Your payment history is the single most important factor in your credit score, making up about 35% of the calculation. Even one late or missed payment can significantly damage your score, especially if it’s reported to the credit bureaus. To avoid this, set up payment reminders, enroll in autopay for at least the minimum amount due, and prioritize paying all bills—credit cards, loans, and utilities—by their due dates.

2. Keep Credit Utilization Low

Credit utilization—the percentage of your available credit that you’re using—is another major factor, contributing to about 30% of your score. Experts recommend keeping your utilization below 30%, but for the best results, aim for 10% or lower. High utilization suggests financial strain, while low utilization shows responsible credit management. To control this, pay down balances before the statement closing date or request a credit limit increase (without increasing spending).

3. Don’t Apply for Too Much Credit at Once

Every time you apply for new credit, a hard inquiry is recorded on your report, which can temporarily lower your score by a few points. Multiple hard inquiries in a short period (such as when shopping for loans or credit cards) can compound this effect, making you appear risky to lenders. Space out applications and only apply for credit when truly necessary.

4. Maintain Older Accounts

The length of your credit history accounts for about 15% of your score. Older accounts demonstrate long-term financial responsibility, so avoid closing them unless absolutely necessary (e.g., high fees). Even if you don’t use an old card often, keeping it open helps your credit age and overall utilization ratio.

5. Use a Mix of Credit Types

Lenders like to see that you can manage different types of credit responsibly. A healthy mix includes:

- Revolving credit (e.g., credit cards)

- Installment loans (e.g., auto loans, mortgages, or personal loans)

While this only makes up about 10% of your score, having a diversified credit profile can give you an edge—just don’t take on debt unnecessarily.

6. Check Your Credit Report Annually

You’re entitled to a free credit report every year from each of the three major bureaus: Equifax, Experian, and TransUnion via AnnualCreditReport.com.

By following these steps consistently, you’ll not only improve your credit score but also maintain it at a strong level, opening doors to better financial opportunities in the future. Patience and discipline are key—good credit is built over time!

Why Might Credit Scores Differ Between Credit Bureaus?

Each credit bureau (Equifax, Experian, and TransUnion) maintains its own file for you. Since not all lenders report to all three bureaus, your credit report—and therefore your score—may differ between them.

Additionally, lenders may use different scoring models depending on the purpose. For example:

- Mortgage lenders may use FICO Score 2 or 5

- Credit card issuers may use FICO Score 8 or VantageScore 4.0

So the “good” score you see in an app may not always be the same one a lender uses.

Final Thoughts: Why a Good Credit Score Is Worth the Effort

Achieving and maintaining a good credit score is one of the smartest financial moves you can make. It’s not just about bragging rights—it’s about unlocking better loan terms, saving on interest, qualifying for apartments, and even securing jobs.

With consistency, smart habits, and the right tools (like rent reporting and credit monitoring), you can build a score that gives you financial freedom and peace of mind. Whether you’re just getting started or rebuilding after a setback, remember: every payment counts, and your score can—and will—improve over time.