What is Soft Credit Check? Working and impact on credit score

When managing your personal finances, especially credit, understanding the different types of credit checks is essential. Whether you’re applying for a loan, checking your own credit score, or receiving pre-approved offers in the mail, chances are your credit is being checked either through a soft inquiry or a hard inquiry.

While most people focus on hard credit checks because they impact your score, soft credit checks are equally important to understand. They can occur without your direct knowledge, and while they don’t hurt your credit score, they do leave a trace on your report.

In this comprehensive guide, we’ll explore what soft credit checks are, how they work, when they happen, and why they matter. Knowing the difference could help you avoid unnecessary stress and take greater control of your financial well-being.

What Is a Soft Inquiries?

A soft credit check, sometimes called a soft inquiry or soft pull, is a type of credit check that happens when someone either you or an institution reviews your credit report for non-lending purposes. Unlike hard inquiries, soft credit checks do not affect your credit score and aren’t visible to lenders or creditors evaluating you for new credit.

These checks are often performed when:

- You check your own credit score or report through a personal finance app

- A lender or credit card issuer checks your credit to determine if you’re eligible for a pre-approved offer

- An employer runs a credit check as part of a job application process

- A landlord screens your creditworthiness before renting to you

- Insurance companies assess your credit to determine policy rates

In all these cases, the inquiry doesn’t signal active credit-seeking behavior, which is why your credit score is not impacted. Soft inquiries are primarily used for informational purposes, and they happen more frequently than most people realize.

What does a soft credit check show?

Soft credit checks work by accessing a limited snapshot of your credit report. They pull information such as your credit score, number of open accounts, and payment history—but they do not go as deep as hard inquiries, which evaluate your full credit file for risk assessment.

For example, if a credit card company wants to send you a pre-approved offer, they’ll conduct a soft inquiry to determine if you meet basic qualifications. They’ll look at high-level metrics like your overall credit score range, existing debt load, and payment reliability.

The same applies when you check your own credit using a free monitoring service. These services typically use soft pulls to retrieve your credit score weekly or monthly without harming your score, giving you the chance to stay informed and make better financial decisions.

What’s important to remember is this: Soft credit checks do not require full consent like hard checks do, but they still require a permissible purpose under the Fair Credit Reporting Act (FCRA), and in some cases such as employment checks written permission is still needed.

Steps by step guide for Soft Credit Check

Here’s a closer look at when and why soft inquiries are made:

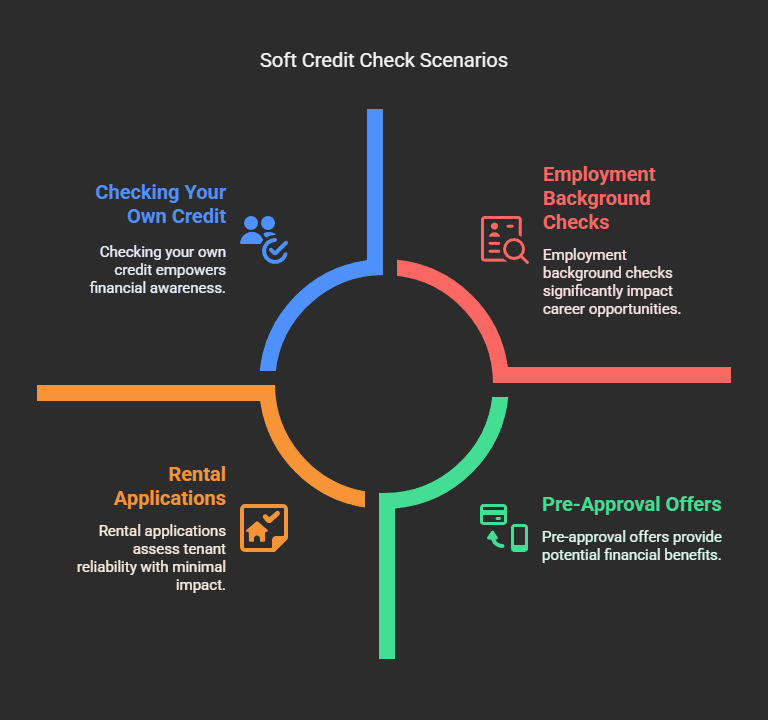

1. Checking Your Own Credit

Using apps like AxcessRent, Credit Karma, NerdWallet, or directly from credit bureaus like Experian or TransUnion, you can check your own score and credit report through a soft inquiry. These checks are unlimited and won’t hurt your credit, no matter how often you do them.

2. Pre-Approval Offers

Banks and lenders may send you pre-approved offers for loans or credit cards based on soft credit checks. These help them identify good potential customers without requiring a full credit application.

3. Employment Background Checks

Certain employers, especially those in finance or government, may conduct credit checks as part of hiring decisions. These are usually soft checks, and they require your written consent.

4. Rental Applications

Landlords and property managers sometimes perform soft inquiries to determine if a tenant has a reliable financial history before approving a lease.

5. Insurance Applications

Auto and homeowners insurance companies may use soft pulls to help set premiums based on credit-based insurance scores.

Understanding when soft inquiries happen helps you stay in control and reduces any surprise when reviewing your credit report.

Soft Credit Check vs. Hard Credit Check

It’s easy to confuse the two, especially because both appear on your credit report. However, the differences are significant and can affect your credit journey.

Here’s a detailed comparison:

| Feature | Soft Credit Check | Hard Credit Check |

|---|---|---|

| Affects Your Credit Score | No | Yes (can lower your score temporarily) |

| Visible to Lenders? | No (only you can see them) | Yes (visible to lenders and financial institutions) |

| Permission Required? | Sometimes (depends on the situation) | Yes (explicit consent is always needed) |

| Purpose | Pre-approval, monitoring, background checks | Credit applications (loans, mortgages, etc.) |

| Duration on Report | 12–24 months (only visible to you) | Up to 2 years (visible to lenders and you) |

| Risk Implication | None | Seen as credit-seeking behavior |

The bottom line is this: soft credit checks are harmless, while hard checks should be limited and timed carefully, especially when applying for a mortgage or auto loan.

Do Soft Credit Checks Require Your Permission?

In most cases, you don’t need to give explicit permission for a soft credit check, especially for pre-approved offers or insurance underwriting. However, the FCRA mandates that companies must have a “permissible purpose” to access your credit—even for a soft pull.

Here are the exceptions where your permission is required:

- Employment credit checks: Always require written consent from the job applicant

- Tenant screening: May require your signature depending on your state’s laws or the rental agency’s policy

While lenders don’t need you to say “yes” for a soft pull when sending you a credit card offer, you still have the right to opt out of pre-screened offers by visiting OptOutPrescreen.com.

Does soft credit check affect credit score?

No, soft credit checks have absolutely no impact on your credit score. You can check your score every day if you want, and it will not lower your score or influence how lenders see you.

This is a major reason why credit monitoring tools are so powerful. They allow you to keep an eye on your financial standing without any consequences. Regular checks also help you spot fraudulent activity or identity theft early because if you see an unfamiliar hard inquiry, you’ll know something’s wrong.

Remember, only hard inquiries which occur when you actively apply for new credit—can lower your score slightly, typically by 5–10 points per inquiry.

Do Soft Inquiries Show Up on My Credit Report?

Yes, but they’re only visible to you, not to lenders or financial institutions.

When you pull your credit report from Equifax, Experian, or TransUnion, there’s a section called “Soft Inquiries” or “Promotional Inquiries.” These entries list every instance when a soft pull was made on your credit profile.

For example:

- “Capital One – Pre-approved Credit Offer”

- “Employer Background Screening – Job Application”

- “You – Credit Monitoring via Credit Karma”

This list is for your records and transparency, not for scoring or evaluation. Lenders will never see or factor in soft inquiries when deciding whether to approve your application.

How Often Can You Have a Soft Credit Check?

There’s no limit to how many soft inquiries you can have. You can check your credit as often as you’d like using free services, and companies can also perform soft pulls regularly for promotional or screening purposes.

In fact, frequent self-monitoring is a good habit, especially if you’re working on improving your credit. Some credit monitoring platforms even notify you of important changes to your credit file, such as:

- New accounts opened

- Changes in your credit utilization

- Missed payments

- Suspicious activity

So go ahead, check your score regularly. It’s safe, smart, and completely free of consequences.

Can a Soft Credit Check Turn Into a Hard Inquiry?

Yes, but only if you take further action.

For example, if you receive a pre-approved credit card offer based on a soft inquiry and then decide to submit a formal application, the lender will conduct a hard inquiry to evaluate your full credit profile. That hard inquiry will then appear on your credit report and could slightly reduce your score.

The key distinction here is intent. Soft inquiries are passive, you’re not actively seeking credit. Hard inquiries signal that you’re trying to borrow money, which is why they impact your score.

So while a soft check won’t hurt you, always be aware that following up with a full application will result in a hard pull.

Final Thoughts

Soft credit checks are one of the safest and most useful tools available to individuals who want to stay informed about their financial health. They allow you to:

- Monitor your score frequently without penalty

- Receive personalized loan and credit offers

- Screen for fraud or identity theft

- Prepare for big purchases by tracking your credit behavior

The more you understand how soft inquiries work, the better equipped you’ll be to protect and grow your credit score. Whether you’re renting a home, applying for a job, or just trying to qualify for the best credit card, knowing what shows up on your report—and what doesn’t—can give you a serious advantage.

Pro tip: You can also build credit without credit cards or loans using services like AxcessRent, which reports on-time rent payments to major credit bureaus. It’s a game-changer for renters looking to improve their credit with no risk of hard inquiries.