What to Do if Your Identity Is Stolen: A Step-by-Step Recovery Guide

Discovering that someone has stolen your identity can feel like your entire life has been flipped upside down. Fraudsters may use your personal information to open credit cards, take out loans, file fake tax returns, or even access your bank accounts. What’s worse—this damage can happen silently for weeks or months before you even realize it.

If you’ve become a victim of identity theft, don’t panic—but do act quickly. The faster you respond, the more you can limit the damage and begin the recovery process. In this comprehensive guide, we’ll walk you through the warning signs of identity theft, the immediate actions you need to take, and how to restore your financial health.

What Is Identity Theft?

Identity theft occurs when someone steals your personal information—like your name, Social Security number, credit card details, or bank account info—and uses it without your permission. This information is then used to commit fraud or other crimes in your name. The consequences can be severe: ruined credit, drained bank accounts, and stressful legal battles.

Common Signs of Identity Theft

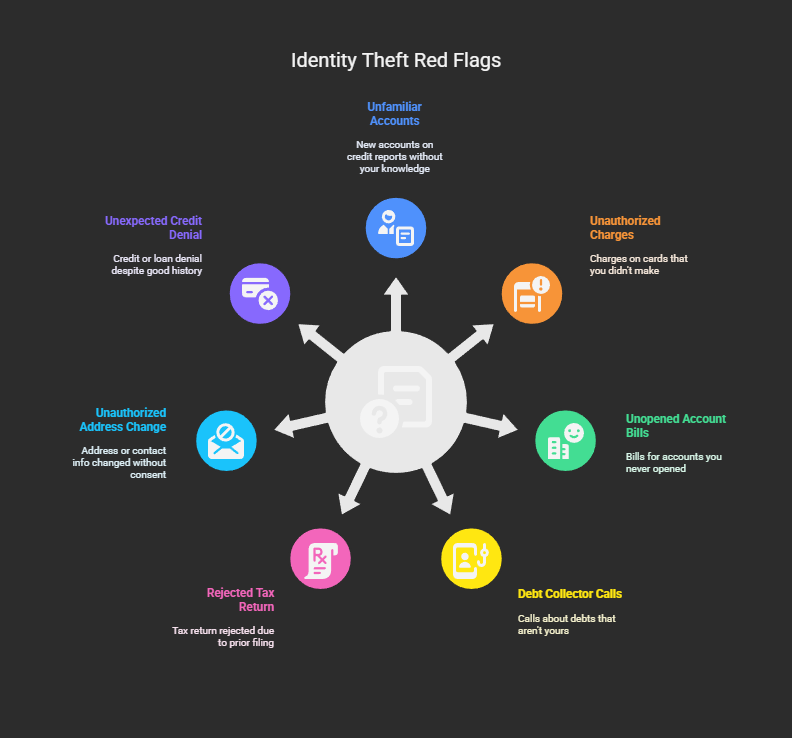

You may not always know right away that your identity has been stolen. Here are some red flags that should raise your suspicion:

- Unfamiliar accounts appear on your credit report

- Unauthorized charges show up on your debit or credit card

- You receive bills or statements for accounts you never opened

- Debt collectors call about debts that aren’t yours

- Your tax return is rejected because one has already been filed

- Your address or contact info is changed without your consent

- You’re denied credit or loans unexpectedly, despite good history

Even something as simple as a piece of suspicious mail can be an early warning. Trust your instincts—if something seems off, take action.

Step 1: Secure Your Credit

One of the first areas identity thieves may target is your credit profile. Here’s what to do:

Place a Fraud Alert

Contact one of the three major credit bureaus (Equifax, Experian, or TransUnion) to request a fraud alert. This will notify any lender pulling your credit to take extra precautions. The bureau you contact must inform the others.

Freeze Your Credit

A credit freeze goes further—it blocks lenders from accessing your credit report entirely, preventing new accounts from being opened in your name.

Check Your Credit Reports

Visit AnnualCreditReport.com and request your free credit reports. Carefully review all activity and flag anything you don’t recognize.

Dispute Fraudulent Activity

If you find accounts or transactions that aren’t yours, file a dispute with each bureau. Include copies of documentation and clearly state why the entry is inaccurate.

Step 2: Report the Identity Theft

The faster you notify the proper authorities, the sooner you can begin reclaiming your identity.

File a Report at IdentityTheft.gov

Visit IdentityTheft.gov and report the theft to the Federal Trade Commission (FTC). This will generate:

- A personalized recovery plan

- Pre-filled dispute letters and forms

- An official Identity Theft Report

This report can be used to help remove fraudulent information from your credit report.

File a Police Report

Depending on the severity, visit your local police department and file a report. Bring your FTC Identity Theft Report, a government ID, proof of address, and any evidence of the theft.

Step 3: Notify Affected Companies

If you know which company or service was compromised—such as your bank, credit card company, or utility provider—contact them immediately. Ask to:

- Close or freeze the account

- Flag it as “fraud” or “compromised”

- Reverse any unauthorized charges

- Issue new cards or account numbers

Most banks and lenders have dedicated fraud departments trained to assist victims of identity theft.

Step 4: Replace Compromised Identification

If documents like your driver’s license, Social Security card, or passport were stolen:

- Contact your local DMV for a replacement driver’s license

- Notify the Social Security Administration if your SSN was misused

- Report a stolen passport to the U.S. Department of State

These documents are often the gateway to more significant forms of fraud, so act quickly.

Step 5: Protect Yourself Going Forward

After you’ve addressed the immediate damage, it’s time to rebuild—and protect yourself from future incidents.

Change All Passwords

Update passwords on all online accounts, especially for banking, email, and e-commerce platforms. Use strong, unique passwords and enable two-factor authentication wherever possible.

Monitor Your Credit Regularly

Sign up for credit monitoring services or use free tools from banks to get alerts on changes to your credit profile.

Opt Out of Pre-Approved Offers

Reduce your risk of fraud by opting out of pre-approved credit and insurance offers at OptOutPrescreen.com.

Keep Personal Info Safe

- Shred sensitive mail

- Don’t carry unnecessary documents (like your Social Security card)

- Never share info on untrusted websites or calls

Summary: Quick Checklist If Your Identity Is Stolen

- Place a fraud alert or credit freeze

- Review and dispute suspicious credit report entries

- Report to the FTC via IdentityTheft.gov

- File a police report (if necessary)

- Contact all affected banks, lenders, and service providers

- Replace any stolen IDs or official documents

- Change all passwords and secure online accounts

- Monitor your credit for ongoing fraud

Final Thoughts

Identity theft is a serious crime—but it doesn’t have to derail your financial future. By acting quickly and following the right steps, you can recover your identity, secure your credit, and move forward with confidence. And remember: prevention is key. Be proactive with your data, stay alert to the signs of fraud, and use tools like credit monitoring and rent reporting services like AxcessRent to strengthen your financial profile.

The sooner you act, the better the outcome—so don’t wait to take control of your identity and your credit.