New FICO Score Model: When Will the New FICO Score Take Effect?

The credit scoring landscape is shifting. For over a decade, the FICO Score 8 model has been the industry standard for most consumer lending (credit cards, personal loans). Meanwhile, the mortgage industry still relies on decades-old versions (FICO 2, 4, and 5).

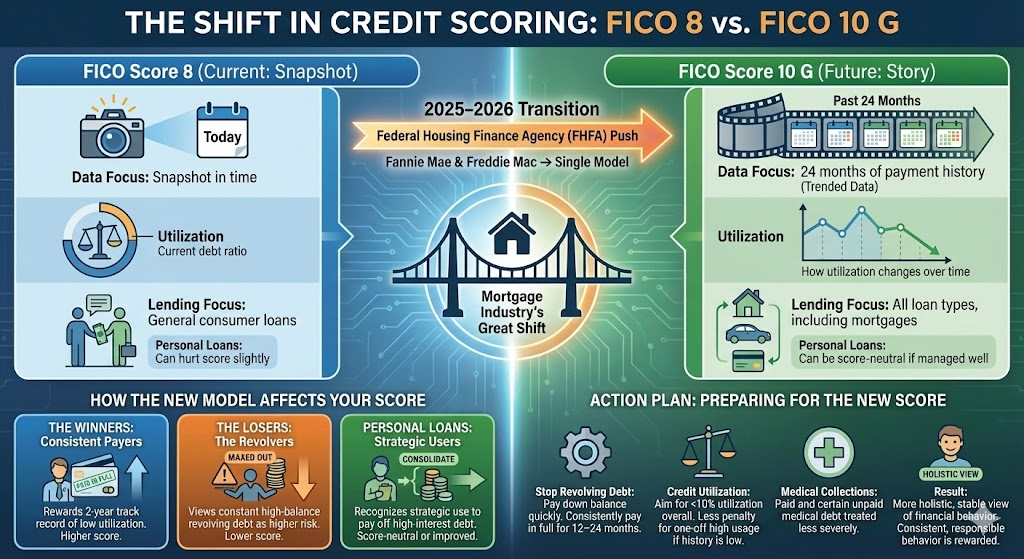

However, New FICO Score has been steadily rolling out its next-generation models, namely FICO Score 10 and the proposed FICO Score 10 G (G for General), which is expected to gain significant traction around 2025-2026. This shift represents the most significant update to how credit risk is calculated in years, offering both opportunities and risks to consumers.

The Core Change: From Snapshot to Story

The primary limitation of the older FICO 8 model is that it takes a snapshot of your credit file on a single day. If you maxed out a credit card, paid it off the next day, and the snapshot happened during that maxed-out period, your score suffered unnecessarily.

The new FICO models are designed to use Trended Data—they look at your credit story over the last 24 months.

Introducing FICO Score 10 G (General)

FICO 10 G is the combination of the FICO 10 and FICO 10 T (Trended Data) models, adapted for mass adoption across all credit bureaus (Experian, TransUnion, Equifax).

| Feature | FICO Score 8 (Current) | FICO Score 10 G (Future) |

|---|---|---|

| Data Focus | Snapshot in time | 24 months of payment history |

| Utilization | Current debt ratio | How utilization changes over time |

| Lending Focus | General consumer loans | All loan types, including mortgages |

| Personal Loans | Can hurt score slightly | Can be score-neutral if managed well |

How the New Model Will Affect Your Score

The shift to Trended Data means your past behavior now dictates your present score more than ever.

1. The Winners: The Consistent Payers

If you consistently pay off your credit card balance in full every month, or frequently pay down your balance, the new model rewards you heavily. The score will see a two-year track record of low utilization, resulting in a higher score.

2. The Losers: The Revolvers

If you constantly carry a high balance (even if you pay the minimum), or repeatedly cycle your credit limits (maxing out, paying down, maxing out again), the score will be lower than it would be under FICO 8. FICO 10 G views constant high-balance revolving debt as a higher risk indicator.

3. Personal Loans

Under FICO 8, taking out a new personal loan (which is often used to pay off high-interest credit card debt) could sometimes cause a temporary score dip because it creates a new “hard inquiry” and a new account. FICO 10 G is designed to recognize and reward users who strategically use installment loans to consolidate and pay off expensive credit card debt.

The Mortgage Industry’s Great Shift

For decades, the mortgage industry has been mandated to use the older FICO models (2, 4, 5), which are stricter and often result in a lower score for the same consumer.

The New Mandate: The Federal Housing Finance Agency (FHFA) has pushed for a major update. The agencies that back the majority of U.S. home loans (Fannie Mae and Freddie Mac) are planning to fully transition away from the “Mortgage Trifecta” (FICO 2, 4, 5) to a single, newer model: FICO Score 10 G.

When Will the New FICO Score Take Effect for Mortgages?

While the mandate is in place, the official transition is a monumental technological task. Lenders need to update their software, train staff, and test millions of loan scenarios.

- Timeline: The transition is expected to occur in phases, with most major lenders adopting FICO 10 G for new mortgage applications around 2025–2026.

This is huge news for homeowners: a single, universal FICO 10 G score means your mortgage score should finally align closely with the FICO score you see on your banking app.

Action Plan: Preparing for the New Score

The best way to prepare for FICO 10 G is to shift your focus from short-term score boosts to long-term financial health.

- Stop Revolving Debt: If you are currently revolving a balance on your credit cards, commit to paying it down as quickly as possible. Consistently paying the statement balance in full for 12–24 months is the single best action you can take.

- Credit Utilization: While utilization is still important, the new score will penalize you less for one-off high usage if the surrounding 24 months show a history of low utilization. Aim for less than 10% utilization overall.

- Medical Collections: FICO 10 G continues the trend of treating paid and certain unpaid medical collection debt less severely than FICO 8. While not an excuse to ignore bills, the negative impact is minimized compared to other forms of debt.

The new FICO 10 G model reflects a more holistic, stable view of financial behavior. Consumers who demonstrate consistent, responsible behavior will likely see their credit scores improve, while those who rely on short-term fixes may find the scoring system less forgiving.

FAQs

What is FICO Score 10 G?

FICO Score 10 G is the general version of FICO’s next model. It mixes FICO Score 10 with trended data from the last 24 months. This looks at your payment trends, not just a one-day snapshot. It will work for most loans, like credit cards and personal loans. Unlike old models, it tracks how your balances change over time.

When will FICO Score 10 G start?

It is set for fall 2025. FICO launched versions with buy-now-pay-later data in June 2025. Lenders will test and use it soon after. For mortgages, the shift to FICO 10 T (trended) and VantageScore 4.0 starts in Q4 2025.

How does FICO 10 G differ from FICO Score 8?

FICO 8 uses a single-day view of your credit. FICO 10 G checks 24 months of data. It weighs personal loans more but can be neutral if you use them to pay off cards. High revolving balances hurt more if they repeat over time. Scores may change by up to 20 points. Most people see small shifts.

Who benefits most from FICO 10 G?

People who pay cards in full each month win big. It shows low use over time, boosting scores. Those who carry balances often lose points. It also helps with debt consolidation via loans. Medical collections get less penalty if paid.

Will my mortgage score change?

Yes. Mortgages now use old FICO 2, 4, or 5. By late 2025, they switch to FICO 10 T. Your score should match what you see on apps better. Aim for steady payments now to prep.

How can I raise my score for FICO 10 G?

Pay cards full each month for 12-24 months. Keep use under 10%. Avoid new debt cycles. Check reports for errors. Build history with on-time rent if reported. Focus on trends, not quick fixes.